Journal of Geographical Sciences >

Chinese investment promoted economic growth while reducing inequality in African countries

|

Guo Tongze, Master Degree, E-mail: guotongze23@mails.ucas.ac.cn |

Received date: 2024-04-05

Accepted date: 2025-04-23

Online published: 2025-08-28

Supported by

National Natural Science Foundation of China(42101424)

National Natural Science Foundation of China(42001115)

Since 2000, China’s investment in Africa has grown rapidly, following a steady upward trajectory. However, this influx of Chinese capital has sparked both economic and political controversies. By integrating multi-source data—from micro-level individual projects to national statistics—this study examines the impact of Chinese investment on African economic development between 2000 and 2022. The results reveal a significant positive correlation between Chinese investment and economic growth across different scales, with investment-intensive regions achieving stronger economic outcomes. The DID analysis indicates that the Belt and Road Initiative has contributed positively to Africa’s economic development. Both static and dynamic panel models confirm that Chinese investment significantly stimulates growth, exhibiting notable lag effects. Furthermore, β-convergence models demonstrate that Chinese investment fosters economic convergence among African countries. Regarding regional inequality, the findings suggest that Chinese investment helps to narrow disparities across Africa, promoting a more balanced economic landscape. Overall, this research underscores the constructive role of China’s investment in fostering economic growth and reducing inequality within the African context.

Key words: Chinese investment; economic growth; regional inequality; Africa

GUO Tongze , DONG Guanpeng , YANG Dongyang , LIU Dexin . Chinese investment promoted economic growth while reducing inequality in African countries[J]. Journal of Geographical Sciences, 2025 , 35(6) : 1263 -1285 . DOI: 10.1007/s11442-025-2366-8

Figure 1 Location and landforms of Africa |

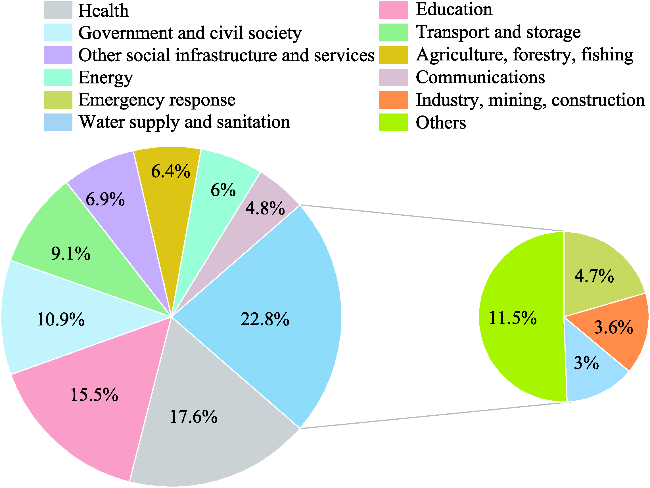

Figure 2 Investment sector distribution |

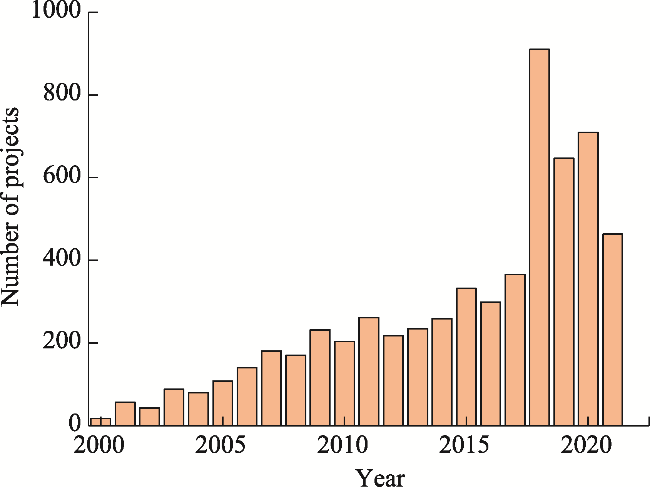

Figure 3 Changes in investment projects |

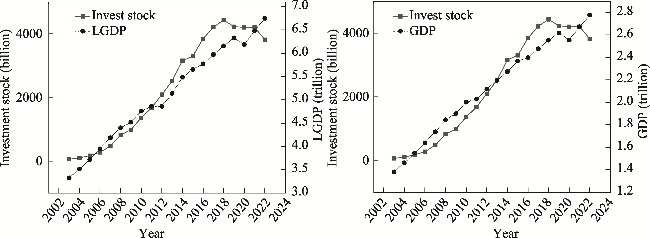

Figure 4 Changes in GDP and investment stock in Africa over the years |

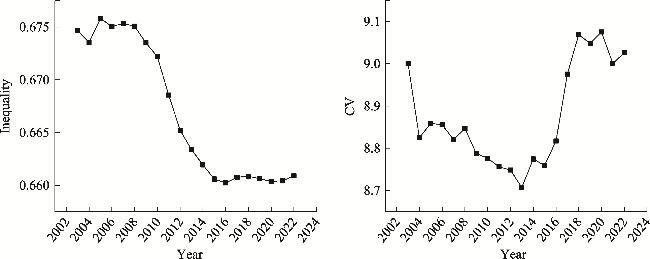

Figure 5 Temporal variation of CV in Africa |

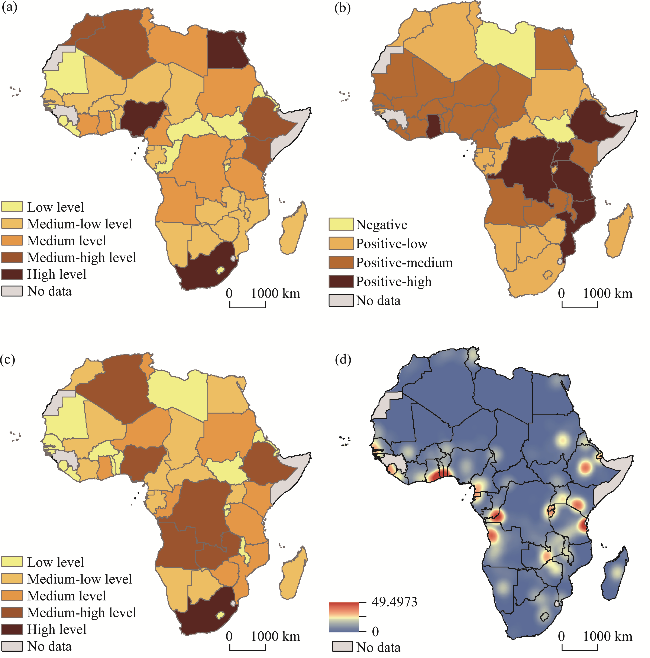

Figure 6 Multi-scale distribution of investment and economic growth: (a) LGDP of African countries in 2022; (b) LGDP growth trend of African countries at the end of the period; (c) Cumulative Chinese investments; (d) Kernel density of investment projects |

Table 1 Multi-scale investment and economic growth correlation |

| Variable | Correlation coefficient | p value | |

|---|---|---|---|

| National scale | Economic growth-Investment stock | 0.175 | p<0.21 |

| Economic growth-Investment density | 0.311 | p<0.03 | |

| Sub-national scale | Economic growth-Investment density | 0.154 | p<0.01 |

| Grid scale (200 km) | Economic growth-Investment density | 0.154 | p<0.01 |

| Buffer zone (200 km) | Economic growth-Investment density | 0.101 | p<0.01 |

| Buffer zone (100 km) | Economic growth-Investment density | 0.067 | p<0.01 |

| Buffer zone (50 km) | Economic growth-Investment density | 0.114 | p<0.01 |

Table 2 Spatial association results of economic growth and investment at different scales |

| Variable | Moran’s I | p value | |

|---|---|---|---|

| National Scale | Economic growth-Investment stock | 0.119 | p<0.05 |

| Economic growth-Investment density | 0.187 | p<0.05 | |

| Sub-national scale | Economic growth-Investment density | 0.100 | p<0.01 |

| Grid-scale (200 km) | Economic growth-Investment density | 0.137 | p<0.05 |

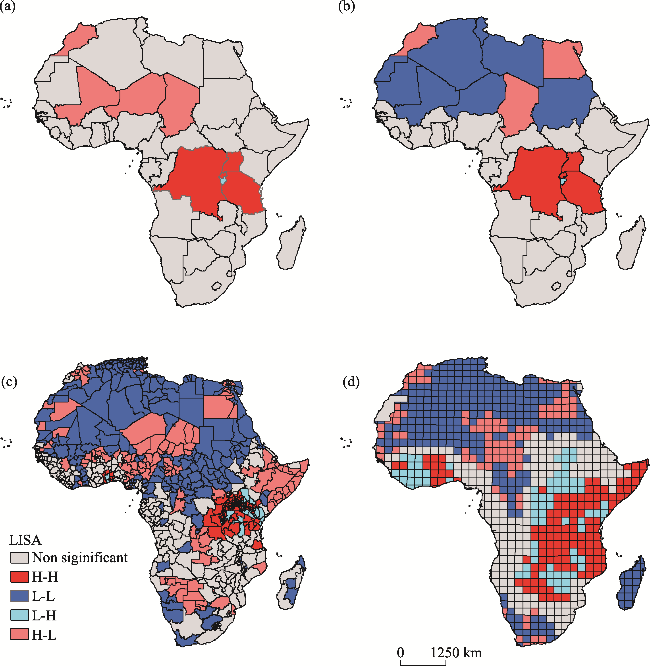

Figure 7 Spatial correlation of economic growth and investment in Africa at multiple scales: (a) National-scale investment stock and economic growth; (b) National-scale investment density and economic growth; (c) Sub-national scale investment density and GDP growth; (d) Grid-scale (200 km) investment density and GDP growth |

Table 3 Results of baseline regression |

| GDP model (1) | GDP model (2) | LGDP model (3) | LGDP model (4) | |

|---|---|---|---|---|

| Constant | 22.483*** | 7.642*** | 24.120*** | 24.140** |

| (150.75) | (5.58) | (2895.73) | (241.37) | |

| tt | 0.314 | 0.852*** | 0.148*** | 0.149*** |

| (0.92) | (3.34) | (7.75) | (8.00) | |

| UPUA | 1.188*** | 0.003 | ||

| (3.23) | (0.107) | |||

| AFFG | 1.878*** | -0.062*** | ||

| (10.92) | (-4.95) | |||

| FTD | 1.408*** | 0.036*** | ||

| (17.85) | (6.28) | |||

| R2 | 0.003 | 0.447 | 0.190 | 0.214 |

| Sample size | 960 | 960 | 960 | 960 |

Note: *** indicates a coefficient is statistically significant (p<0.01); ** indicates a coefficient is statistically significant (p<0.05); * indicates a coefficient is statistically significant (p<0.1). |

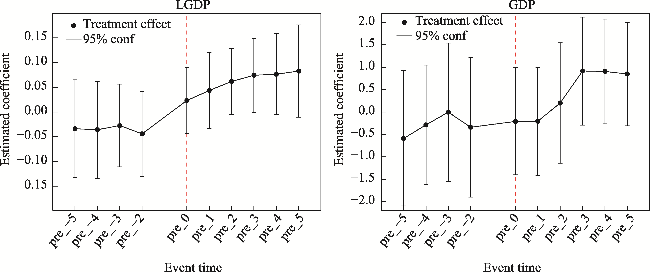

Figure 8 The results of parallel trend |

Table 4 The results of PSM |

| Treat | Control | Std (%) | t | p value | ||

|---|---|---|---|---|---|---|

| UPUA | Before | 3.728 | 3.614 | 22.46 | 3.448 | 0.001 |

| After | 3.728 | 3.699 | 6.20 | 0.817 | 0.414 | |

| AFFG | Before | 2.643 | 2.719 | -7.54 | -1.147 | 0.252 |

| After | 2.643 | 2.593 | 4.72 | 0.576 | 0.565 | |

| FTD | Before | 3.724 | 3.758 | -2.54 | -0.388 | 0.698 |

| After | 3.724 | 3.771 | -3.47 | -0.429 | 0.666 |

Note: *** indicates a coefficient is statistically significant (p<0.01); ** indicates a coefficient is statistically significant (p<0.05); * indicates a coefficient is statistically significant (p<0.1). |

Table 5 PSM-DID regression results |

| GDP model (1) | GDP model (2) | LGDP model (3) | LGDP model (4) | |

|---|---|---|---|---|

| tt | -0.085 | 0.653*** | 0.194*** | 0.192*** |

| (-0.21) | (2.13) | (8.60) | (8.63) | |

| Constant term | 22.721*** | 7.972*** | 24.280*** | 24.324*** |

| (115.95) | (5.378) | (2208.44) | (241.64) | |

| Control variables | No | Yes | No | Yes |

| Sample size | 960 | 960 | 960 | 960 |

| R2 | -0.002 | 0.462 | 0.293 | 0.317 |

Note: *** indicates a coefficient is statistically significant (p<0.01); ** indicates a coefficient is statistically significant (p<0.05); * indicates a coefficient is statistically significant (p<0.1). |

Figure 9 The results of placebo test |

Table 6 Static panel and dynamic panel |

| LGDP Static panel | GDP Static panel | LGDP Dynamic panel | GDP Dynamic panel | |

|---|---|---|---|---|

| Constant | 22.989*** | 16.143*** | 23.152*** | 16.514** |

| (184.30) | (52.53) | (189.15) | (49.83) | |

| Invest | 0.078*** | 0.047*** | 0.024*** | 0.018*** |

| (22.05) | (12.86) | (2.82) | (2.87) | |

| Investn-1 | 0.054*** | 0.030*** | ||

| (7.28) | (5.19) | |||

| UPUA | 0.161*** | 1.893*** | 0.020*** | 1.791*** |

| (4.80) | (21.65) | (3.69) | (18.95) | |

| AFFG | -0.062*** | -0.068*** | -0.057*** | -0.074*** |

| (-3.75) | (-5.16) | (-3.53) | (-5.60) | |

| FTD | 0.017** | 0.010 | 0.018** | 0.011* |

| (2.41) | (1.57) | (2.55) | (1.65) | |

| R2 | 0.411 | 0.684 | 0.398 | 0.697 |

| Sample size | 960 | 960 | 912 | 912 |

Note: *** indicates a coefficient is statistically significant (p<0.01); ** indicates a coefficient is statistically significant (p<0.05); * indicates a coefficient is statistically significant (p<0.1). |

Table 7 β-convergence model |

| Absolute β | Conditional β | Absolute β (light) | Conditional β (light) | |

|---|---|---|---|---|

| Constant term | 4.346*** | -1.222 | 0.960*** | 1.225*** |

| (20.61) | (-0.33) | (6.87) | (8.08) | |

| Invest | 0.032*** | 0.002** | ||

| (4.11) | (2.08) | |||

| GDPi-1 | -0.610*** | -0.768*** | -0.077*** | -0.092*** |

| (-20.55) | (-25.20) | (-6.81) | (-7.30) | |

| UPUA | 1.267*** | -0.021*** | ||

| (13.08) | (-3.17) | |||

| AFFG | 0.089*** | -0.014*** | ||

| (2.80) | (-4.42) | |||

| FTD | 0.097*** | 0.004*** | ||

| (7.10) | (2.63) | |||

| R2 | 0.297 | 0.504 | 0.360 | 0.357 |

| Sample size | 960 | 960 | 960 | 960 |

Note: *** indicates a coefficient is statistically significant (p<0.01); ** indicates a coefficient is statistically significant (p<0.05); * indicates a coefficient is statistically significant (p<0.1). |

Table 8 CV and inequality model |

| CVgdp | CVgdp_per_capita | Inequality | CVgdp | CVgdp_per_capita | Inequality | ||

|---|---|---|---|---|---|---|---|

| Constant term | 8.159*** | 28.51*** | 0.690*** | AFFG | 0.272*** | 0.017 | 0.010*** |

| (16.55) | (264.71) | (38.80) | (4.18) | (1.20) | (4.12) | ||

| Invest | 0.011 | -0.011*** | -0.002*** | FTD | 0.018 | -0.002 | -0.003*** |

| (0.81) | (-3.71) | (-3.43) | (0.63) | (-0.24) | (-2.73) | ||

| UPUA | -0.049 | -0.028 | -0.006 | R2 | 0.025 | 0.021 | 0.041 |

| (-0.37) | (-0.97) | (-1.28) | Sample size | 960 | 960 | 960 |

Note: *** indicates a coefficient is statistically significant (p<0.01); ** indicates a coefficient is statistically significant (p<0.05); * indicates a coefficient is statistically significant (p<0.1). |

| [1] |

|

| [2] |

African Union Commission, OECD, 2018. Africa’s Development Dynamics 2018: Growth, Jobs and Inequalities. Addis Ababa and Paris/AUC: OECD Publishing.

|

| [3] |

|

| [4] |

|

| [5] |

|

| [6] |

|

| [7] |

|

| [8] |

|

| [9] |

|

| [10] |

|

| [11] |

|

| [12] |

|

| [13] |

|

| [14] |

|

| [15] |

|

| [16] |

|

| [17] |

|

| [18] |

|

| [19] |

|

| [20] |

|

| [21] |

|

| [22] |

|

| [23] |

|

| [24] |

|

| [25] |

|

| [26] |

|

| [27] |

|

| [28] |

|

| [29] |

|

| [30] |

|

| [31] |

|

| [32] |

|

| [33] |

|

| [34] |

|

| [35] |

|

| [36] |

|

| [37] |

|

| [38] |

|

| [39] |

|

| [40] |

|

| [41] |

|

| [42] |

|

| [43] |

|

| [44] |

|

| [45] |

|

| [46] |

|

| [47] |

Suyanto,

|

| [48] |

|

| [49] |

|

| [50] |

|

| [51] |

|

| [52] |

|

| [53] |

|

| [54] |

|

| [55] |

|

/

| 〈 |

|

〉 |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}