Journal of Geographical Sciences >

Dynamics of the global semiconductor trade and its dependencies

|

Ren Yawen (1992-), PhD Candidate, specialized in industrial geography and regional development. E-mail: renyw.19b@igsnrr.ac.cn |

Received date: 2022-12-22

Accepted date: 2023-02-10

Online published: 2023-06-26

Supported by

National Natural Science Foundation of China(42130712)

The semiconductor industry typifies the international division of labor and exhibits significant structural differences in global trade in key product segments. The evolution of cross-border trade flows and dependency relationships, as well as trade organization patterns of manufactured products, equipment and materials for manufacturing, are investigated by constructing a global semiconductor trade relationship matrix and using the Gini coefficient and trade dependency index. It was found that: (1) the global semiconductor trade is highly spatially unbalanced, with materials and equipment trade in particular highly concentrated in a few countries on both the supply and demand sides; (2) China has replaced the US as the largest global semiconductor trade player and has shaped the regionalized system of manufactured goods and materials trade with East and Southeast Asian economies, but its equipment trade is highly dependent on Europe and the US; (3) the semiconductor production model has promoted the regionalization of the east and southeast Asia region in the trade of manufactured products and materials, and developed economies such as the US, the EU, Japan, and South Korea have maintained their monopolistic advantage in the trade of semiconductor equipment by building exclusive innovation networks and establishing trade barriers. The monopolistic nature of the semiconductor equipment trade and the regionalization of manufactured goods and materials have formed the characteristics of the global semiconductor trade and are likely to be further strengthened in future trade.

REN Yawen , YANG Yu , WANG Yun , LIU Yi . Dynamics of the global semiconductor trade and its dependencies[J]. Journal of Geographical Sciences, 2023 , 33(6) : 1141 -1160 . DOI: 10.1007/s11442-023-2123-9

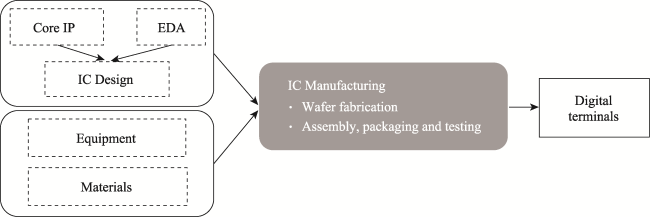

Figure 1 Semiconductor manufacturing chain |

Table 1 Commodity attributes of semiconductors in international trade |

| Product Categories | Products | HS Code | Description of product content |

|---|---|---|---|

| Semiconductor manufactured goods | Integrated circuit devices | 8541 | Diodes, transistors, similar semiconductor devices; including light-emitting diodes (LEDs), mounted piezoelectric crystals, assembled or unassembled in modules or panels |

| Integrated circuits and microelectronic components | 8542 | Electronic integrated circuits | |

| Key equipment for semiconductor manufacturing | Photolithography/ | 848620 | Machines and equipment used individually or primarily for the manufacture of semiconductor ingots or wafers, semiconductor devices, electronic integrated circuits or flat-panel displays |

| etching machines | 848620 | ||

| Ion injectors | 848620/854311 | ||

| Key materials for semiconductor manufacturing | Printed circuit boards | 8534 | Printed circuits |

| Silicon wafers | 3818 | Chemical elements doped for use in electronic products, in the form of discs, wafers or the like; compounds doped for use in electronic products; including gallium nitride wafers, silicon wafers | |

| Silicon raw materials | 280461 | Silicon; containing not less than 99.99% silicon by weight | |

| Silicon raw materials | 280469 | Silicon; containing less than 99.99% by weight of silicon | |

| Photoresist | 370710 | For integrated circuits and semiconductor discrete devices, exposure micro-imaging process | |

| Electronic gases | 280429 | Rare gases for semiconductor production | |

| Electronic special gases | 280430 | Nitrogen for semiconductor production |

Table 2 Gini coefficient of global semiconductor trade |

| 1999 | 2009 | 2019 | ||||

|---|---|---|---|---|---|---|

| Export | Import | Export | Import | Export | Import | |

| Manufactured goods | 0.9501 | 0.9301 | 0.9445 | 0.9326 | 0.9473 | 0.9323 |

| Manufacturing materials | 0.9354 | 0.9164 | 0.9458 | 0.9278 | 0.9472 | 0.9222 |

| Manufacturing equipment | 0.9878 | 0.9698 | 0.9740 | 0.9654 | 0.9739 | 0.9739 |

Table 3 Changes in the trade value and proportion of semiconductor manufactured goods in key economies |

| Unit | 1999 | 2009 | 2019 | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| % | Export | Specific gravity | Import | Specific gravity | Export | Specific gravity | Import | Specific gravity | Export | Specific gravity | Import | Specific gravity |

| China | 66.09 | 1.54 | 137.15 | 3.2 | 930.11 | 12.02↑ | 1676.98 | 21.76↑ | 2477.62 | 16.47↑ | 3387.09 | 22.64↑ |

| China Taiwan | 151.04 | 3.52 | 184.98 | 4.31 | 521.37 | 6.74↑ | 267.11 | 3.47↓ | 1337.05 | 8.89↑ | 480.12 | 3.21↓ |

| Korea | 369.84 | 8.62 | 288.83 | 6.73 | 815.27 | 10.53↑ | 509.4 | 6.61↓ | 2015.63 | 13.4↑ | 831.52 | 5.56↓ |

| United States | 993.82 | 23.16 | 766.87 | 17.88 | 769.44 | 9.94↓ | 469 | 6.09↓ | 1047.7 | 6.96↓ | 816.28 | 5.46↓ |

| Japan | 622.19 | 14.5 | 255.85 | 5.97 | 792.56 | 10.24 | 355 | 4.61↓ | 1081.27 | 7.19↓ | 474.65 | 3.17↓ |

| Germany | 159.2 | 3.71 | 205.46 | 4.79 | 298.99 | 3.86↑ | 409.21 | 5.31↑ | 526.85 | 3.5↓ | 670.74 | 4.48↓ |

| Netherlands | 48.14 | 1.12 | 71.83 | 1.7 | 105.02 | 1.36↑ | 126.58 | 1.64↓ | 221.52 | 1.47↑ | 336.02 | 2.25↑ |

| United Kingdom | 103.73 | 2.42 | 160.18 | 3.74 | 46.89 | 0.61 | 41.35 | 0.54↓ | 74.84 | 0.5↓ | 74.81 | 0.5↓ |

| Malaysia | 371.8 | 8.67 | 388.73 | 9.06 | 723.95 | 9.35↑ | 502.58 | 6.52↓ | 1786.5 | 11.87↑ | 757.3 | 5.06↓ |

| Singapore | 514.33 | 11.99 | 579.8 | 13.52 | 1390.48 | 17.97↑ | 1036.76 | 13.45↓ | 1936.05 | 12.87↓ | 1617.19 | 10.81↓ |

Note: The unit of import and export is USD billion, the unit of proportion is %, and ↓ and ↑ represent the increase and decrease of import and export trade volume compared with the previous nodal year respectively. |

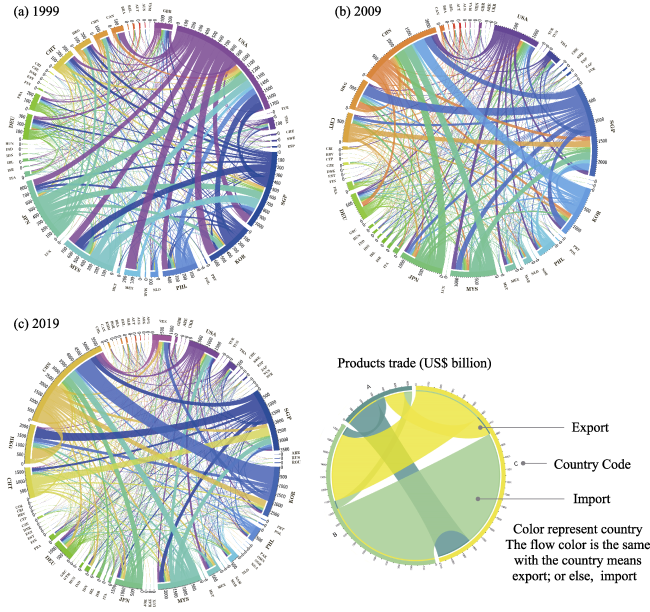

Figure 2 Global trade flow of semiconductor manufactured goods |

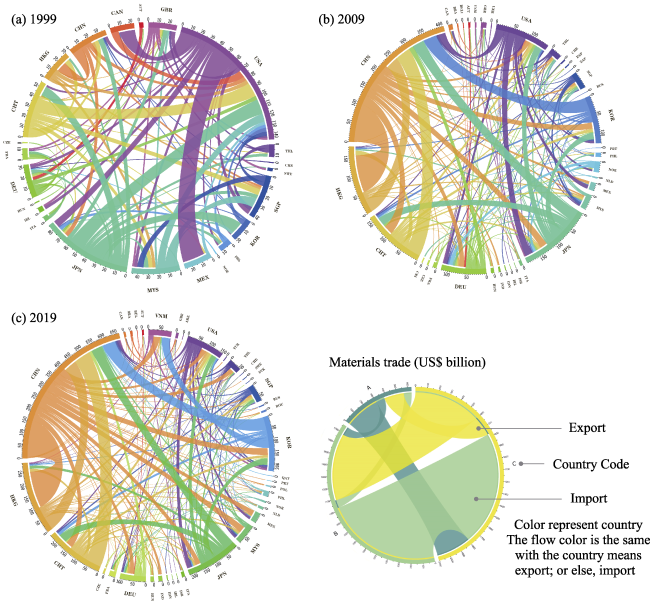

Figure 3 Global trade flow of semiconductor materials |

Table 4 Changes in the trade value and proportion of semiconductor materials in key economies |

| Unit | 1999 | 2009 | 2019 | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| % | Export | Specific gravity | Import | Specific gravity | Export | Specific gravity | Import | Specific gravity | Export | Specific gravity | Import | Specific gravity |

| China | 27.59 | 6.38 | 20.42 | 4.71 | 277.89 | 26.91↑ | 234.86 | 22.86↑ | 419.98 | 29.7↑ | 270.35 | 19.16↑ |

| China Taiwan | 48.27 | 11.15 | 16.79 | 3.88 | 106.77 | 10.34↓ | 73.8 | 7.18↑ | 151.22 | 10.69↓ | 98.71 | 7↓ |

| Korea | 14.59 | 3.37 | 17.14 | 3.96 | 75.12 | 7.27↑ | 62.07 | 6.04↑ | 132.54 | 9.37↑ | 98.48 | 6.98↑ |

| United States | 79.14 | 18.29 | 78.98 | 18.24 | 98.16 | 9.51↓ | 71.62 | 6.97↓ | 83.04 | 5.87↓ | 98.22 | 6.96↓ |

| Japan | 71.25 | 16.46 | 26.11 | 6.03 | 136.02 | 13.17↓ | 77.29 | 7.52↑ | 172.44 | 12.2↓ | 66.61 | 4.72↓ |

| Germany | 24.18 | 5.59 | 25.05 | 5.78 | 63.13 | 6.11↑ | 70.74 | 6.88↑ | 58 | 4.1↓ | 64.07 | 4.54↓ |

| Netherlands | 2.46 | 0.57 | 5.54 | 1.28 | 4.79 | 0.46↓ | 8.24 | 0.8↓ | 7.76 | 0.55↑ | 12.3 | 0.87↑ |

| United Kingdom | 14.69 | 3.39 | 22.5 | 5.2 | 11.31 | 1.1↓ | 14.97 | 1.46↓ | 8.49 | 0.6↓ | 16.77 | 1.19↓ |

| Malaysia | 27.57 | 6.37 | 25.72 | 5.94 | 15.45 | 1.5↓ | 35 | 3.41↓ | 27.5 | 1.94↑ | 66.01 | 4.68↑ |

| Singapore | 16.4 | 3.79 | 33.28 | 7.68 | 26.01 | 2.52↓ | 30.85 | 3↓ | 33.09 | 2.34↓ | 46.2 | 3.27↑ |

Note: The unit of import and export is USD billion, the unit of proportion is %, and ↓ and ↑ respectively represent the increase and decrease of import and export trade volume compared with the previous period. |

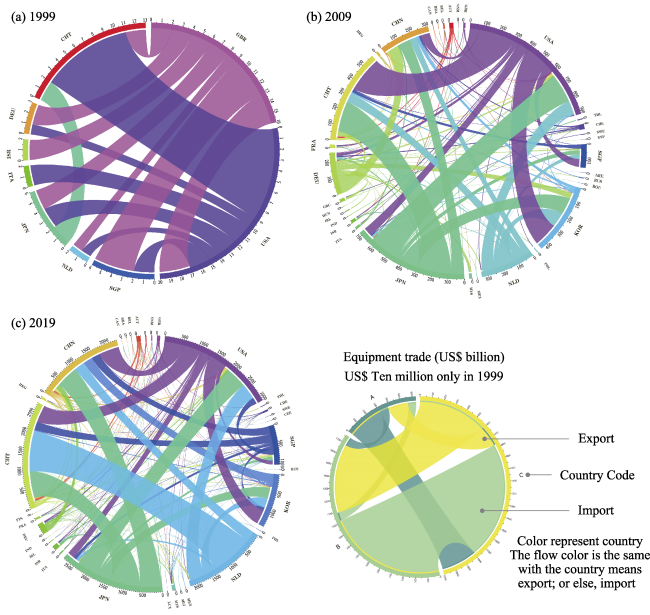

Figure 4 Global trade flow of semiconductor equipment |

Table 5 Changes in the trade value and proportion of semiconductor equipment in key economies |

| Unit | 1999 | 2009 | 2019 | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| % | Export | Specific gravity | Import | Specific gravity | Export | Specific gravity | Import | Specific gravity | Export | Specific gravity | Import | Specific gravity |

| China | 0 | 0 | 0 | 0 | 1.15 | 0.56↑ | 31.14 | 15.2↑ | 15.34 | 1.84↑ | 216.58 | 25.86↑ |

| China Taiwan | 0 | 0 | 1.24 | 32.46 | 1.87 | 0.91↑ | 57 | 27.83↓ | 17.06 | 2.04↑ | 264.02 | 31.52↑ |

| Korea | 0 | 0 | 0 | 0 | 4.9 | 2.39↑ | 40.12 | 19.59↑ | 35.74 | 4.28↑ | 105.38 | 12.58↓ |

| United States | 1.8 | 47 | 0.34 | 8.9 | 61.17 | 29.86 | 31.97 | 15.61↑ | 177.59 | 21.26↓ | 131.13 | 15.66↑ |

| Japan | 0.21 | 5.48 | 0.41 | 10.73 | 63.73 | 31.11↑ | 8.73 | 4.26↓ | 235.79 | 28.23↓ | 39.24 | 4.69↑ |

| Germany | 0.02 | 0.52 | 0.31 | 8.12 | 21.49 | 10.49↑ | 5.72 | 2.79↓ | 21.81 | 2.61↓ | 7.88 | 0.94↓ |

| Netherlands | 0.07 | 1.83 | 0.26 | 6.81 | 33.25 | 16.23↑ | 1.14 | 0.56↓ | 215.49 | 25.8↑ | 4 | 0.48↓ |

| United Kingdom | 1.7 | 44.39 | 0.02 | 0.52 | 1.15 | 0.56↓ | 0.54 | 0.26↓ | 7.8 | 0.93↑ | 1.21 | 0.14↓ |

| Malaysia | 0 | 0 | 0 | 0 | 0.31 | 0.15↑ | 1.94 | 0.95↑ | 3.26 | 0.39↑ | 6.33 | 0.76↓ |

| Singapore | 0.01 | 0.26 | 0.68 | 17.8 | 3.32 | 1.62↑ | 11.96 | 5.84↓ | 77.36 | 9.26↑ | 26.59 | 3.17↓ |

Note: The unit of import and export is USD billion, the unit of proportion is %, and ↓ and ↑ respectively represent the increase and decrease of import and export trade volume compared with the previous period. |

Table 6 HM index of manufactured goods trade between key economies (top 10) |

| Place of production | Place of consumption | HM1999 | Place of production | Place of consumption | HM2009 | Place of production | Place of consumption | HM2019 |

|---|---|---|---|---|---|---|---|---|

| Malaysia | Singapore | 0.29 | Korea | China | 0.36 | Israel | China | 0.53 |

| Korea | United States | 0.28 | Malaysia | China | 0.31 | Korea | China | 0.45 |

| China Taiwan | United States | 0.25 | Japan | China | 0.3 | China Taiwan | Singapore | 0.34 |

| Malaysia | United States | 0.23 | China Taiwan | Singapore | 0.29 | Japan | China | 0.31 |

| China Taiwan | Singapore | 0.19 | Malaysia | Singapore | 0.22 | Malaysia | China | 0.24 |

| Japan | United States | 0.18 | Korea | Singapore | 0.19 | United States | China | 0.22 |

| Singapore | United States | 0.18 | United States | China | 0.15 | Malaysia | Singapore | 0.16 |

| China | United States | 0.16 | Singapore | China | 0.14 | Singapore | China | 0.15 |

| Japan | Singapore | 0.16 | United States | Malaysia | 0.12 | Korea | Vietnam | 0.11 |

| Singapore | Malaysia | 0.15 | Germany | Malaysia | 0.11 | Germany | China | 0.1 |

Table 7 HM index of semiconductor materials trade between key economies (top 10) |

| Place of production | Place of consumption | HM1999 | Place of production | Place of consumption | HM2009 | Place of production | Place of consumption | HM2019 |

|---|---|---|---|---|---|---|---|---|

| Korea | United States | 0.30 | Korea | China | 0.45 | China Taiwan | China | 0.41 |

| Malaysia | United States | 0.27 | China Taiwan | China | 0.36 | Korea | China | 0.35 |

| China Taiwan | United States | 0.27 | Japan | China | 0.21 | Japan | China | 0.23 |

| Malaysia | Singapore | 0.27 | Singapore | Malaysia | 0.20 | Malaysia | Singapore | 0.20 |

| Singapore | Malaysia | 0.23 | Singapore | Korea | 0.18 | Singapore | Korea | 0.19 |

| Singapore | United States | 0.23 | United States | China | 0.17 | Malaysia | China | 0.19 |

| Japan | United States | 0.19 | Malaysia | Singapore | 0.16 | Japan | China Taiwan | 0.17 |

| Japan | Korea | 0.14 | United States | Japan | 0.15 | Singapore | China Taiwan | 0.15 |

| China | United States | 0.13 | Malaysia | United States | 0.14 | Japan | Korea | 0.14 |

| China Taiwan | Singapore | 0.12 | Japan | China Taiwan | 0.14 | Singapore | China | 0.12 |

Table 8 HM index of semiconductor equipment trade between key economies (top 10) |

| Place of consumption | Place of production | HM 1999 | Place of consumption | Place of production | HM 2009 | Place of consumption | Place of production | HM 2019 |

|---|---|---|---|---|---|---|---|---|

| China Taiwan | Japan | 0.86 | China Taiwan | Singapore | 0.61 | China | Korea | 0.71 |

| China Taiwan | United States | 0.48 | China | Korea | 0.39 | China Taiwan | Netherlands | 0.52 |

| Singapore | United Kingdom | 0.24 | China Taiwan | United States | 0.38 | China | Germany | 0.50 |

| United States | United Kingdom | 0.20 | China | Germany | 0.34 | China Taiwan | Japan | 0.30 |

| Israel | United Kingdom | 0.14 | China Taiwan | Japan | 0.31 | China Taiwan | Singapore | 0.29 |

| Singapore | United States | 0.13 | Korea | Netherlands | 0.29 | United States | Japan | 0.28 |

| Japan | United States | 0.12 | United States | Netherlands | 0.26 | China | United Kingdom | 0.28 |

| China Taiwan | United Kingdom | 0.12 | Korea | United States | 0.25 | China | Japan | 0.25 |

| Japan | United Kingdom | 0.10 | United States | Japan | 0.23 | United States | United Kingdom | 0.22 |

| Germany | United Kingdom | 0.09 | Korea | Germany | 0.18 | United States | Korea | 0.21 |

Figure 5 Geographical model evolution in the semiconductor trade space model |

| Country name | ISO-3 | Country name | ISO-3 | Country name | ISO-3 | Country name | ISO-3 | |||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Afghanistan | AFG | Algeria | DZA | Saint Lucia | LCA | Rwanda | RWA | |||||

| Angola | AGO | Ecuador | ECU | Liechtenstein | LIE | Saudi Arabia | SAU | |||||

| Albania | ALB | Egypt | EGY | Sri Lanka | LKA | Sudan | SDN | |||||

| Andorra | AND | Eritrea | ERI | Lesotho | LSO | Senegal | SEN | |||||

| United Arab Emirates | ARE | Spain | ESP | Lithuania | LTU | Singapore | SGP | |||||

| Argentina | ARG | Estonia | EST | Luxembourg | LUX | Solomon Islands | SLB | |||||

| Armenia | ARM | Ethiopia | ETH | Latvia | LVA | Sierra Leone | SLE | |||||

| Antigua and Barbuda | ATG | Finland | FIN | Morocco | MAR | El Salvador | SLV | |||||

| Australia | AUS | Fiji | FJI | Monaco | MCO | San Marino | SMR | |||||

| Austria | AUT | France | FRA | Moldova | MDA | Somalia | SOM | |||||

| Azerbaijan | AZE | Micronesia | FSM | Madagascar | MDG | Serbia | SRB | |||||

| Burundi | BDI | Gabon | GAB | Maldives | MDV | South Sudan | SSD | |||||

| Belgium | BEL | United Kingdom | GBR | Mexico | MEX | Sao Tome and Principe | STP | |||||

| Benin | BEN | Georgia | GEO | Marshall Islands | MHL | Suriname | SUR | |||||

| Burkina Faso | BFA | Ghana | GHA | North Macedonia | MKD | Slovakia | SVK | |||||

| Bangladesh | BGD | Guinea | GIN | Mali | MLI | Slovenia | SVN | |||||

| Bulgaria | BGR | Gambia | GMB | Malta | MLT | Sweden | SWE | |||||

| Bahrain | BHR | Guinea-Bissau | GNB | Myanmar | MMR | Swaziland | SWZ | |||||

| Bahamas | BHS | Equatorial Guinea | GNQ | Montenegro | MNE | Seychelles | SYC | |||||

| Bosnia and Herzegovina | BIH | Greece | GRC | Mongolia | MNG | Syria | SYR | |||||

| Belarus | BLR | Grenada | GRD | Mozambique | MOZ | Chad | TCD | |||||

| Belize | BLZ | Guatemala | GTM | Mauritania | MRT | Togo | TGO | |||||

| Bolivia | BOL | Guyana | GUY | Mauritius | MUS | Thailand | THA | |||||

| Brazil | BRA | Honduras | HND | Malawi | MWI | Tajikistan | TJK | |||||

| Barbados | BRB | Croatia | HRV | Malaysia | MYS | Turkmenistan | TKM | |||||

| Brunei | BRN | Haiti | HTI | Namibia | NAM | Timor-Leste | TLS | |||||

| Bhutan | BTN | Hungary | HUN | Niger | NER | Tonga | TON | |||||

| Botswana | BWA | Indonesia | IDN | Nigeria | NGA | Trinidad and Tobago | TTO | |||||

| Central African Republic | CAF | India | IND | Nicaragua | NIC | Tunisia | TUN | |||||

| Canada | CAN | Ireland | IRL | Niue | NIU | Turkey | TUR | |||||

| Switzerland | CHE | Iran | IRN | Netherlands | NLD | Tuvalu | TUV | |||||

| Chile | CHL | Iraq | IRQ | Norway | NOR | Tanzania | TZA | |||||

| China | CHN | Iceland | ISL | Nepal | NPL | Uganda | UGA | |||||

| Côte d’Ivoire | CIV | Israel | ISR | Nauru | NRU | Ukraine | UKR | |||||

| Cameroon | CMR | Italy | ITA | New Zealand | NZL | Uruguay | URY | |||||

| Democratic Republic of the Congo | COD | Jamaica | JAM | Oman | OMN | United States of America | USA | |||||

| Republic of the Congo | COG | Jordan | JOR | Pakistan | PAK | Uzbekistan | UZB | |||||

| Cook Islands | COK | Japan | JPN | Panama | PAN | Holy See | VAT | |||||

| Colombia | COL | Kazakhstan | KAZ | Peru | PER | Saint Vincent and the Grenadines | VCT | |||||

| Comoros | COM | Kenya | KEN | Philippines | PHL | Venezuela | VEN | |||||

| Cape Verde | CPV | Kyrgyzstan | KGZ | Palau | PLW | Vietnam | VNM | |||||

| Costa Rica | CRI | Cambodia | KHM | Papua New Guinea | PNG | Vanuatu | VUT | |||||

| Cuba | CUB | Kiribati | KIR | Poland | POL | Samoa | WSM | |||||

| Cyprus | CYP | Saint Kitts and Nevis | KNA | Democratic People’s Republic of Korea | PRK | Yemen | YEM | |||||

| Czech Republic | CZE | Republic of Korea | KOR | Portugal | PRT | South Africa | ZAF | |||||

| Germany | DEU | Kuwait | KWT | Paraguay | PRY | Zambia | ZMB | |||||

| Djibouti | DJI | Laos | LAO | Palestine | PSE | Zimbabwe | ZWE | |||||

| Dominica | DMA | Lebanon | LBN | Qatar | QAT | |||||||

| Denmark | DNK | Liberia | LBR | Romania | ROU | |||||||

| Dominican Republic | DOM | Libya | LBY | Russia | RUS | |||||||

| [1] |

|

| [2] |

|

| [3] |

|

| [4] |

|

| [5] |

|

| [6] |

|

| [7] |

|

| [8] |

|

| [9] |

|

| [10] |

|

| [11] |

|

| [12] |

|

| [13] |

|

| [14] |

|

| [15] |

|

| [16] |

|

| [17] |

|

| [18] |

|

| [19] |

|

| [20] |

|

| [21] |

|

| [22] |

|

| [23] |

|

| [24] |

|

| [25] |

|

| [26] |

|

| [27] |

|

| [28] |

|

| [29] |

|

| [30] |

|

| [31] |

|

| [32] |

|

| [33] |

|

| [34] |

|

| [35] |

|

| [36] |

|

| [37] |

|

| [38] |

|

| [39] |

|

| [40] |

|

/

| 〈 |

|

〉 |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}