Journal of Geographical Sciences >

The impact of COVID-19 on China’s regional economies and industries

|

Wu Feng (1979–), PhD and Associate Professor, specialized in complex system modeling and sustainable development. E-mail: wufeng@igsnrr.ac.cn |

Received date: 2020-12-01

Accepted date: 2021-01-29

Online published: 2021-06-25

Supported by

National Natural Science Foundation of China, No(72042020)

Copyright

Scientifically assessing the economic impact of major public health emergencies, containing their negative effects, and enhancing the resilience of an economy are important national strategic needs. The new coronavirus disease (COVID-19) has, to date, been effectively contained in China, but the threat of imported cases and local risks still exist. The systematic identification of the virus’s path of influence and intensity is significant for economic recovery. This study is based on a refined multi-regional general equilibrium analysis model, which measures the economic and industrial impacts at different epidemic risk levels in China and simulates development trends and the degree of damage to industries and the economy under changes to supplies of production materials and product demand. The results show that, at the macroeconomic level, China’s GDP will decline about 0.4% to 0.8% compared to normal in 2020, with an average drop of about 2% in short-term consumption, an average drop in employment of about 0.7%, and an average increase in prices of about 0.9%. At the industry level, the epidemic will have the greatest short-term impact on consumer and labor- intensive industries. For example, the output value of the service industry will fall 6.3% compared to normal. Looking at the impact of the epidemic on the industrial system, the province most affected by the epidemic is Hubei, which is the only province in China in the level-1 risk category. As the disease spread outward from Hubei, there were clear differences in the main industries that were impacted in different regions. In addition, simulation results of recovery intensity of regional economies under the two epidemic response scenarios of resumption of work and production and active fiscal stimulus policies show that an increase in fiscal stimulus policies produces a 0.3% higher rate of gross regional product growth but it causes commodity prices to rise by about 1.8%. Measures to resume work and production offer a wider scope for industrial recovery.

WU Feng , LIU Guijun , GUO Naliang , LI Zhihui , DENG Xiangzheng . The impact of COVID-19 on China’s regional economies and industries[J]. Journal of Geographical Sciences, 2021 , 31(4) : 565 -583 . DOI: 10.1007/s11442-021-1859-3

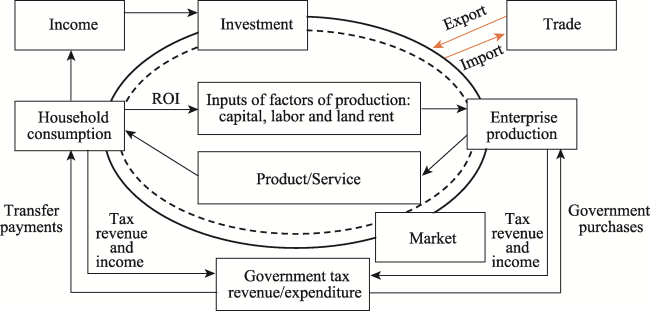

Figure 1 The enormous regional model (TERM) framework |

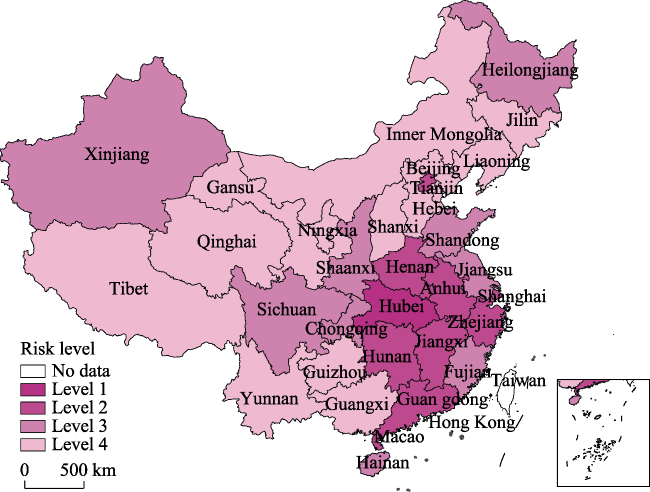

Table 1 Statistics of COVID-19 risk classification in China |

| Confirmed cases (number) | Total population (million) | Levels 1-2 (days) | Levels 2-3 (days) | Levels 1-3 (days) | Outflow of population (%) | Risk level classification | |

|---|---|---|---|---|---|---|---|

| Hubei | 68139 | 59.17 | 99 | 44 | 143 | 0.00 | 1 |

| Guangdong | 1758 | 113.46 | 32 | 75 | 107 | 8.07 | 2 |

| Zhejiang | 1278 | 57.37 | 39 | 21 | 60 | 2.97 | 2 |

| Henan | 1276 | 96.05 | 54 | 47 | 101 | 19.22 | 2 |

| Hunan | 1019 | 68.99 | 47 | 21 | 68 | 16.82 | 2 |

| Anhui | 991 | 63.24 | 32 | 19 | 51 | 6.74 | 2 |

| Beijing | 935 | 21.54 | 97 | 37 | 134 | 1.44 | 2 |

| Jiangxi | 935 | 46.48 | 48 | 8 | 56 | 7.86 | 2 |

| Shanghai | 913 | 24.24 | 60 | 46 | 106 | 1.36 | 2 |

| Heilongjiang | 948 | 37.73 | 39 | 21 | 60 | 0.45 | 3 |

| Chongqing | 583 | 31.02 | 46 | 14 | 60 | 8.40 | 3 |

| Xinjiang | 902 | 24.87 | 31 | 11 | 42 | 0.24 | 3 |

| Jiangsu | 665 | 80.51 | 31 | 32 | 63 | 3.84 | 3 |

| Shandong | 831 | 100.47 | 44 | 59 | 103 | 2.18 | 3 |

| Sichuan | 656 | 83.41 | 33 | 28 | 61 | 4.14 | 3 |

| Fujian | 384 | 39.41 | 33 | 22 | 55 | 2.52 | 3 |

| Shaanxi | 373 | 38.64 | 0 | 0 | 34 | 3.28 | 3 |

| Hainan | 171 | 9.34 | 0 | 0 | 32 | 0.89 | 3 |

| Hebei | 365 | 75.56 | 97 | 37 | 134 | 1.87 | 4 |

| Inner Mongolia | 261 | 25.34 | 0 | 0 | 31 | 0.26 | 4 |

| Tianjin | 230 | 15.60 | 97 | 37 | 134 | 0.23 | 4 |

| Liaoning | 263 | 43.59 | 0 | 0 | 28 | 0.46 | 4 |

| Guangxi | 257 | 49.26 | 0 | 0 | 31 | 1.86 | 4 |

| Shanxi | 203 | 37.18 | 30 | 15 | 45 | 1.20 | 4 |

| Gansu | 169 | 26.37 | 0 | 0 | 27 | 0.71 | 4 |

| Yunnan | 199 | 48.30 | 0 | 0 | 31 | 1.12 | 4 |

| Ningxia | 75 | 6.88 | 34 | 68 | 102 | 0.07 | 4 |

| Jilin | 157 | 27.04 | 32 | 23 | 55 | 0.28 | 4 |

| Guizhou | 147 | 36.00 | 0 | 0 | 30 | 1.40 | 4 |

| Qinghai | 18 | 6.03 | 0 | 0 | 32 | 0.08 | 4 |

| Tibet | 1 | 3.44 | 36 | 22 | 58 | 0.02 | 4 |

Figure 2 COVID-19 risk classification in China |

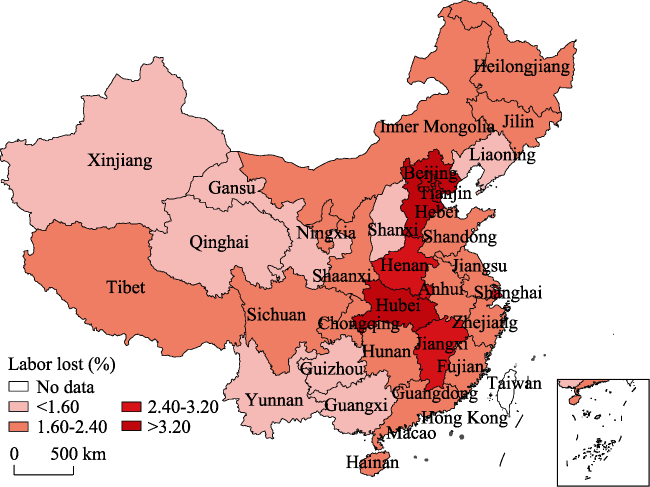

Figure 3 Estimations of labor losses caused by COVID-19 containment measures in China |

Table 2 Scenario design and parameters for economic impact and adaptation analysis of COVID-19 epidemic |

| Scenario design | Impact Scenario 1 | Impact Scenario 2 (+Scenario 1) | Impact Scenario 3 (+Scenario 2) | Impact Scenario 4 (+Scenario 3) | Adaptive Scenario 1 (+Scenario 4) | Adaptive Scenario 2 (+Scenario 4) |

|---|---|---|---|---|---|---|

| Shock conditions | Declining labor supply | Transportation controls | Equal decline in industrial demand of all regions | Equal reduction in exports of all regions | Return to work and production | Government expenditure |

| a. Health and social work | ||||||

| b. Information transmission and technology | ||||||

| c. Accommodation and catering | ||||||

| d. Wholesale and retail | ||||||

| f. Entertainment | ||||||

| Level-1 areas | -3.20% | -53% | a. 18.2% | -1% | 1.12% | 13.08% |

| b. 9.7% | ||||||

| Level-2 areas | -2.40% | -34% | c. -18.0% | -1% | 0.96% | 18.70% |

| Level-3 areas | -1.60% | -30% | d. -7.5% | -1% | 0.64% | 15.00% |

| Level-4 areas | -1.20% | -26% | f. -9.0% | -1% | 0.48% | 10.00% |

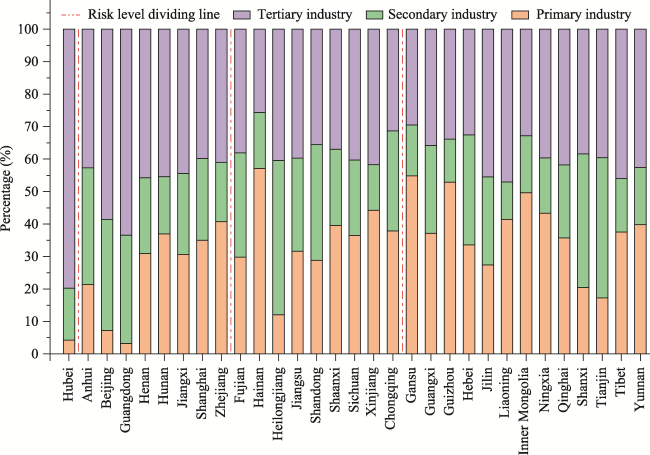

Figure 4 Employment ratios in industrial sectors of each Chinese province in 2019 |

Table 3 Rates of change in GRP, CPI, employment rate, household consumption, imports and exports under different COVID-19 containment scenarios (%) |

| Macro indicators | GRP | CPI | Employment | Household consumption | Imports | Exports |

|---|---|---|---|---|---|---|

| Ⅰ. ‒0.768 | Ⅰ. 1.101 | Ⅰ. ‒1.387 | Ⅰ. ‒2.575 | Ⅰ. 0.142 | Ⅰ. ‒0.935 | |

| Level-1 areas | Ⅱ. ‒0.786 | Ⅱ. 1.243 | Ⅱ. ‒1.381 | Ⅱ. ‒2.432 | Ⅱ. -0.331 | Ⅱ. ‒0.939 |

| Ⅲ. ‒0.796 | Ⅲ. 1.113 | Ⅲ. ‒1.339 | Ⅲ. ‒2.710 | Ⅲ. ‒0.544 | Ⅲ. ‒0.734 | |

| Ⅳ. ‒0.810 | Ⅳ. 1.010 | Ⅳ. ‒1.347 | Ⅳ. ‒2.178 | Ⅳ. ‒0.686 | Ⅳ. ‒0.744 | |

| Level-2 areas | Ⅰ. ‒0.546 | Ⅰ. 0.910 | Ⅰ. ‒1.045 | Ⅰ. ‒2.577 | Ⅰ. 0.035 | Ⅰ. ‒0.644 |

| Ⅱ. ‒0.546 | Ⅱ. 0.979 | Ⅱ. ‒1.044 | Ⅱ. ‒2.514 | Ⅱ. ‒0.036 | Ⅱ. ‒0.629 | |

| Ⅲ. ‒0.514 | Ⅲ. 1.004 | Ⅲ. ‒0.881 | Ⅲ. ‒2.408 | Ⅲ. 0.100 | Ⅲ. ‒0.456 | |

| Ⅳ. ‒0.530 | Ⅳ. 0.897 | Ⅳ. ‒0.894 | Ⅳ. ‒1.860 | Ⅳ. ‒0.041 | Ⅳ. -0.465 | |

| Level-3 areas | Ⅰ. ‒0.356 | Ⅰ. 0.882 | Ⅰ. ‒0.676 | Ⅰ. ‒3.032 | Ⅰ. 0.142 | Ⅰ. ‒0.527 |

| Ⅱ. ‒0.355 | Ⅱ. 0.962 | Ⅱ. ‒0.671 | Ⅱ. -2.951 | Ⅱ. 0.060 | Ⅱ. ‒0.519 | |

| Ⅲ. ‒0.366 | Ⅲ. 0.755 | Ⅲ. ‒0.573 | Ⅲ. ‒3.194 | Ⅲ. 0.115 | Ⅲ. ‒0.280 | |

| Ⅳ. ‒0.378 | Ⅳ. 0.654 | Ⅳ. ‒0.581 | Ⅳ. ‒2.141 | Ⅳ. ‒0.010 | Ⅳ. ‒0.299 | |

| Level-4 areas | Ⅰ. ‒0.236 | Ⅰ. 0.870 | Ⅰ. ‒0.479 | Ⅰ. ‒3.073 | Ⅰ. 0.342 | Ⅰ. ‒0.417 |

| Ⅱ. ‒0.240 | Ⅱ. 0.929 | Ⅱ. ‒0.478 | Ⅱ. ‒3.021 | Ⅱ. 0.267 | Ⅱ. ‒0.394 | |

| Ⅲ. ‒0.284 | Ⅲ. 0.647 | Ⅲ. ‒0.402 | Ⅲ. ‒3.380 | Ⅲ. 0.256 | Ⅲ. ‒0.077 | |

| Ⅳ. ‒0.294 | Ⅳ. 0.549 | Ⅳ. ‒0.408 | Ⅳ. ‒2.216 | Ⅳ. 0.133 | Ⅳ. ‒0.091 |

Note: I is impact scenario 1; II is impact scenario 2; III is impact scenario 3; and IV is impact scenario 4. Source: TERM-China model simulation results |

Table 4 Rates of change in output of major sectors of secondary industry under different COVID-19 containment scenarios (%) |

| Sector | Level-1 areas | Level-2 areas | Level-3 areas | Level-4 areas |

|---|---|---|---|---|

| Textiles | Ⅰ. ‒1.852 | Ⅰ. ‒1.329 | Ⅰ. ‒1.061 | Ⅰ. ‒0.943 |

| Ⅱ. ‒1.846 | Ⅱ. ‒1.320 | Ⅱ. ‒1.051 | Ⅱ. -0.908 | |

| Ⅲ. -1.708 | Ⅲ. ‒1.105 | Ⅲ. ‒0.527 | Ⅲ. ‒0.179 | |

| Ⅳ. ‒1.744 | Ⅳ. ‒1.132 | Ⅳ. ‒0.563 | Ⅳ. ‒0.218 | |

| Clothing, shoes, hats and leather and down products | Ⅰ. ‒1.283 | Ⅰ. ‒1.105 | Ⅰ. ‒0.896 | Ⅰ. -0.732 |

| Ⅱ. ‒1.134 | Ⅱ. -1.066 | Ⅱ. -0.860 | Ⅱ. ‒0.662 | |

| Ⅲ. ‒1.244 | Ⅲ. ‒0.935 | Ⅲ. ‒0.432 | Ⅲ. ‒0.054 | |

| Ⅳ. ‒1.264 | Ⅳ. ‒0.959 | Ⅳ. ‒0.465 | Ⅳ. ‒0.086 | |

| Wood products and furniture | Ⅰ. ‒1.316 | Ⅰ. ‒0.981 | Ⅰ. ‒0.712 | Ⅰ. ‒0.600 |

| Ⅱ. ‒1.303 | Ⅱ. ‒0.972 | Ⅱ. ‒0.708 | Ⅱ. ‒0.577 | |

| Ⅲ. ‒1.356 | Ⅲ. ‒1.025 | Ⅲ. -0.585 | Ⅲ. ‒0.352 | |

| Ⅳ. ‒1.380 | Ⅳ. ‒1.045 | Ⅳ. ‒0.611 | Ⅳ. ‒0.379 | |

| Papermaking, printing and cultural, educational and sporting goods | Ⅰ. ‒1.361 | Ⅰ. ‒1.008 | Ⅰ. ‒0.746 | Ⅰ. ‒0.642 |

| Ⅱ. ‒1.380 | Ⅱ. ‒1.016 | Ⅱ. ‒0.758 | Ⅱ. ‒0.635 | |

| Ⅲ. ‒1.411 | Ⅲ. ‒1.056 | Ⅲ. ‒0.595 | Ⅲ. ‒0.353 | |

| Ⅳ. ‒1.437 | Ⅳ. ‒1.078 | Ⅳ. ‒0.621 | Ⅳ. ‒0.380 | |

| Communication equipment, computers and other electronic equipment | Ⅰ. ‒1.291 | Ⅰ. ‒1.152 | Ⅰ. ‒0.957 | Ⅰ. ‒0.790 |

| Ⅱ. ‒1.259 | Ⅱ. ‒1.157 | Ⅱ. ‒0.962 | Ⅱ. ‒0.785 | |

| Ⅲ. ‒1.281 | Ⅲ. ‒1.123 | Ⅲ. ‒0.850 | Ⅲ. ‒0.638 | |

| Ⅳ. ‒1.338 | Ⅳ. ‒1.168 | Ⅳ. ‒0.893 | Ⅳ. ‒0.662 | |

| Instrumentation | Ⅰ. ‒1.128 | Ⅰ. ‒0.954 | Ⅰ. ‒0.804 | Ⅰ. ‒0.719 |

| Ⅱ. ‒1.154 | Ⅱ. ‒0.965 | Ⅱ. ‒0.819 | Ⅱ. ‒0.730 | |

| Ⅲ. ‒1.130 | Ⅲ. -0.927 | Ⅲ. -0.700 | Ⅲ. ‒0.593 | |

| Ⅳ. ‒1.137 | Ⅳ. ‒0.936 | Ⅳ. ‒0.705 | Ⅳ. ‒0.590 | |

| Other manufacturing products | Ⅰ. ‒1.385 | Ⅰ. ‒0.880 | Ⅰ. ‒0.730 | Ⅰ. ‒0.602 |

| Ⅱ. ‒1.409 | Ⅱ. ‒0.876 | Ⅱ. ‒0.728 | Ⅱ. ‒0.590 | |

| Ⅲ. ‒1.436 | Ⅲ. ‒0.895 | Ⅲ. ‒0.652 | Ⅲ. ‒0.488 | |

| Ⅳ. ‒1.484 | Ⅳ. ‒0.921 | Ⅳ. ‒0.681 | Ⅳ. -0.511 |

Note: I is impact Scenario 1; II is impact Scenario 2; III is impact Scenario 3; and IV is impact Scenario 4. |

Table 5 Rates of change in output of major sectors of tertiary industry under different COVID-19 containment scenarios (%) |

| Sector | Level-1 areas | Level-2 areas | Level-3 areas | Level-4 areas |

|---|---|---|---|---|

| Wholesale and retail | Ⅰ. ‒0.875 | Ⅰ. ‒0.667 | Ⅰ. ‒0.460 | Ⅰ. ‒0.293 |

| Ⅱ. ‒0.904 | Ⅱ. ‒0.662 | Ⅱ. ‒0.454 | Ⅱ. ‒0.285 | |

| Ⅲ. ‒1.213 | Ⅲ. ‒2.117 | Ⅲ. ‒2.134 | Ⅲ. ‒2.478 | |

| Ⅳ. ‒1.226 | Ⅳ. ‒2.128 | Ⅳ. ‒2.146 | Ⅳ. ‒2.486 | |

| Transportation, storage and postal services | Ⅰ. ‒0.706 | Ⅰ. ‒0.574 | Ⅰ. ‒0.422 | Ⅰ. ‒0.347 |

| Ⅱ. ‒1.261 | Ⅱ. ‒0.749 | Ⅱ. -0.610 | Ⅱ. ‒0.523 | |

| Ⅲ. ‒1.277 | Ⅲ. ‒0.727 | Ⅲ. ‒0.598 | Ⅲ. ‒0.531 | |

| Ⅳ. ‒1.293 | Ⅳ. ‒0.744 | Ⅳ. ‒0.613 | Ⅳ. ‒0.545 | |

| Accommodation and catering | Ⅰ. -0.671 | Ⅰ. ‒0.601 | Ⅰ. ‒0.387 | Ⅰ. ‒0.360 |

| Ⅱ. ‒0.472 | Ⅱ. ‒0.551 | Ⅱ. ‒0.333 | Ⅱ. ‒0.314 | |

| Ⅲ. ‒4.833 | Ⅲ. -4.146 | Ⅲ. ‒4.221 | Ⅲ. -3.770 | |

| Ⅳ. ‒4.827 | Ⅳ. ‒4.146 | Ⅳ. ‒4.218 | Ⅳ. ‒3.768 | |

| Information transmission, software and IT services | Ⅰ. ‒0.419 | Ⅰ. ‒0.330 | Ⅰ. ‒0.177 | Ⅰ. ‒0.118 |

| Ⅱ. ‒0.407 | Ⅱ. ‒0.314 | Ⅱ. ‒0.160 | Ⅱ. ‒0.108 | |

| Ⅲ. 1.034 | Ⅲ. 1.175 | Ⅲ. 1.433 | Ⅲ. 1.458 | |

| Ⅳ. 1.034 | Ⅳ. 1.173 | Ⅳ. 1.433 | Ⅳ. 1.458 | |

| Rental and Business Services | Ⅰ. -0.927 | Ⅰ. ‒0.840 | Ⅰ. ‒0.582 | Ⅰ. ‒0.514 |

| Ⅱ. ‒0.970 | Ⅱ. ‒0.858 | Ⅱ. ‒0.605 | Ⅱ. ‒0.529 | |

| Ⅲ. ‒1.053 | Ⅲ. -1.020 | Ⅲ. -0.721 | Ⅲ. ‒0.650 | |

| Ⅳ. ‒1.054 | Ⅳ. ‒1.029 | Ⅳ. ‒0.724 | Ⅳ. ‒0.655 | |

| Health and social work | Ⅰ. ‒0.180 | Ⅰ. ‒0.139 | Ⅰ. ‒0.026 | Ⅰ. 0.018 |

| Ⅱ. 0.144 | Ⅱ. ‒0.049 | Ⅱ. 0.070 | Ⅱ. 0.100 | |

| Ⅲ. 10.606 | Ⅲ. 9.281 | Ⅲ. 9.406 | Ⅲ. 8.736 | |

| Ⅳ. 10.610 | Ⅳ. 9.283 | Ⅳ. 9.411 | Ⅳ. 8.740 | |

| Culture, sports and entertainment | Ⅰ. ‒0.610 | Ⅰ. ‒0.717 | Ⅰ. ‒0.471 | Ⅰ. ‒0.390 |

| Ⅱ. ‒0.425 | Ⅱ. ‒0.702 | Ⅱ. ‒0.447 | Ⅱ. ‒0.367 | |

| Ⅲ. ‒3.472 | Ⅲ. ‒2.346 | Ⅲ. ‒2.324 | Ⅲ. ‒2.024 | |

| Ⅳ. ‒3.457 | Ⅳ. ‒2.341 | Ⅳ. ‒2.316 | Ⅳ. ‒2.016 |

Note: I is impact Scenario 1; II is impact Scenario 2; III is impact Scenario 3; and IV is impact Scenario 4. |

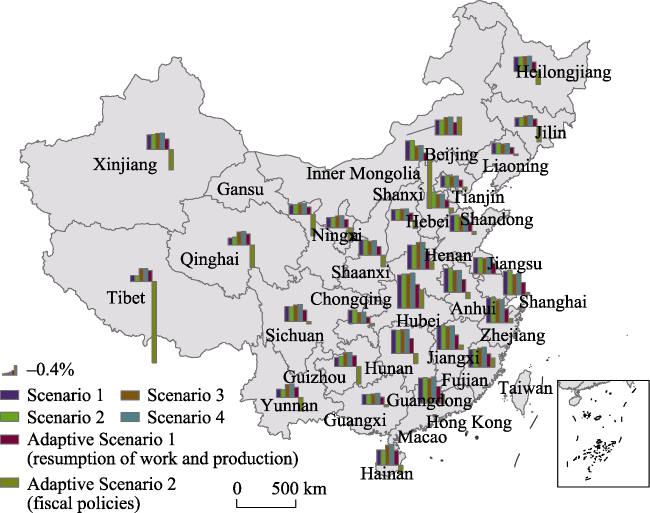

Figure 5 Rates of change in GRP of each province under different COVID-19 epidemic containment scenarios |

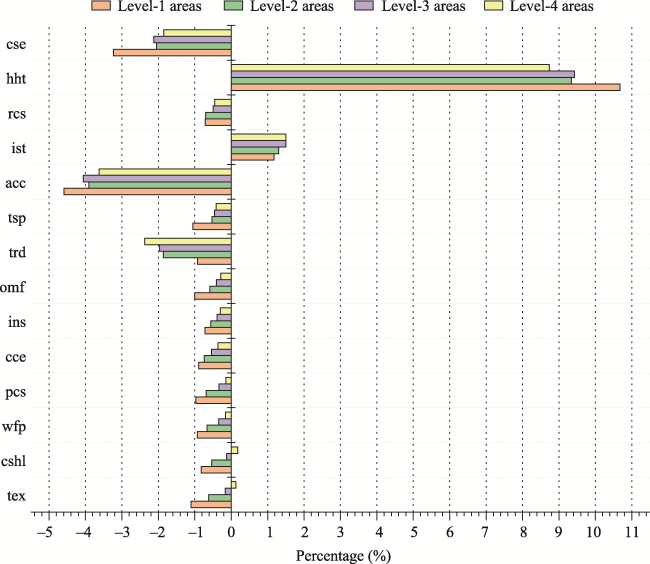

Figure 6 Rates of change in output of major sectors of regions with different COVID-19 risks under adaptive scenario 1 |

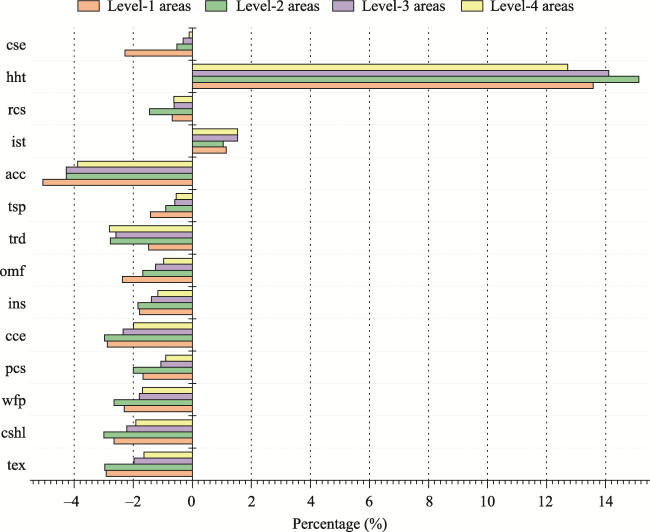

Figure 7 Rates of change in output of major sectors of regions with different COVID-19 risks under adaptive scenario 2Note: cse-Culture, sports and entertainment; hht-Health and social work; rcs-Rental and commercial services; ist-Information transmission, software and IT services; acc-Accommodation and catering; tsp-Transportation, storage and postal services; trd-Wholesale and retail; omf-Other manufacturing products; ins-Instrumentation; cce-Communication equipment, computers and other electronic equipment; pcs-Papermaking, printing and cultural and sporting goods; wfp-Wood products and furniture; cshl-Clothing, shoes, hats and leather and down products; tex-Textiles |

| 1 |

|

| 2 |

|

| 3 |

|

| 4 |

|

| 5 |

|

| 6 |

|

| 7 |

|

| 8 |

|

| 9 |

|

| 10 |

|

| 11 |

|

| 12 |

|

| 13 |

|

| 14 |

|

| 15 |

|

| 16 |

|

| 17 |

|

| 18 |

|

| 19 |

|

| 20 |

|

| 21 |

|

| 22 |

|

| 23 |

|

| 24 |

|

| 25 |

|

| 26 |

|

| 27 |

|

| 28 |

|

| 29 |

|

| 30 |

|

| 31 |

|

| 32 |

|

| 33 |

|

| 34 |

|

| 35 |

|

| 36 |

|

| 37 |

|

| 38 |

|

| 39 |

|

| 40 |

|

| 41 |

|

| 42 |

|

| 43 |

|

| 44 |

|

| 45 |

|

| 46 |

|

| 47 |

|

| 48 |

|

| 49 |

|

/

| 〈 |

|

〉 |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}