Journal of Geographical Sciences >

Energy geopolitics in Central Asia: China’s involvement and responses

|

Zhou Qiang (1986–), PhD Candidate, specialized in economic geography and regional studies. E-mail: littlesir@sina.com |

Received date: 2020-03-31

Accepted date: 2020-06-23

Online published: 2021-01-25

Supported by

National Natural Science Foundation of China(4187118)

Foundation: National Natural Science Foundation of China(42022007)

The Strategic Priority Research Program of the CAS(XDA20040400)

Copyright

To ensure adequate oil supply and mitigate geopolitical uncertainties, China has diversified its sources of crude oil imports in recent years. Central Asia is a neighbor region of China, rich in oil and natural gas reserves, which can play an important role in China’s strategy to reduce its dependence on energy supplies from the Middle East. The geopolitical attributes of energy and the geopolitical situation in Central Asia determine that Central Asia’s energy development and cooperation are disturbed by domestic and foreign factors, and also face the risks of complex energy structural evolution and geopolitical games, which create a unique energy geopolitical pattern in Central Asia. This study proposes an analysis framework for energy geopolitics in Central Asia, arguing that the complexity of energy geopolitics in Central Asia can be demonstrated from the perspectives of both the main countries of energy development (game actors) and the whole-industry-chain of energy development (game themes). The most obvious feature of Central Asian energy geopolitics is the fierce game that is played between key countries and regions, Russia, the United States, China, the European Union (EU), Japan, India, Iran, and Turkey. Strategic geopolitical considerations and resource requirements necessitate the active participation of these players in Central Asian energy development and mean that the foreign policy agendas of states in this region are likely to become ever more crowded. Therefore, the energy cooperation between China and Central Asia faces the geopolitical risks of the great power games. It is necessary to develop reasonable and effective policies to establish guarantee mechanisms to minimize the risks of energy cooperation. This study characterizes the energy geopolitical strategies of Russia, the United States, China, and other related powers in Central Asia. It also assesses the country risks faced by energy cooperation between China and Central Asian countries. To withstand possible geopolitical and country risks, this study develops a series of policy frameworks which can be used to fortify the stability of the energy cooperation between China and Central Asian countries, and can also be effective in responding to the array of risks that might be encountered in the coming years.

ZHOU Qiang , HE Ze , YANG Yu . Energy geopolitics in Central Asia: China’s involvement and responses[J]. Journal of Geographical Sciences, 2020 , 30(11) : 1871 -1895 . DOI: 10.1007/s11442-020-1816-6

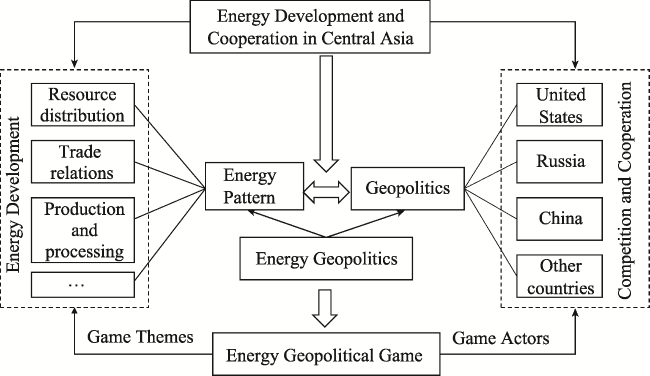

Figure 1 The analysis framework of energy geopolitics in Central Asia |

Table 1 Gas purchases in Central Asia by Gazprom Group (billion cubic meters) |

| Countries | 2014 | 2015 | 2016 | 2017 | 2018 |

|---|---|---|---|---|---|

| For supplies to Europe | |||||

| Turkmenistan | 11.0 | 3.1 | - | - | - |

| Uzbekistan | 3.6 | 3.5 | 4.3 | 5.5 | 3.8 |

| Kazakhstan | 10.9 | 12.6 | 12.7 | 13.8 | 12.3 |

| For supplies to southern Kazakhstan | |||||

| Uzbekistan | 3.7 | 2.9 | 1.9 | 1.7 | 2.9 |

| For supplies to Kyrgyzstan | |||||

| Uzbekistan | 0.04 | 0.0* | 0.0* | 0.0* | 0.0* |

| Kazakhstan | 0.06 | 0.2 | 0.2 | 0.3 | 0.3 |

Source: Gazprom website, https://www.gazprom.com/about/marketing/cis-baltia/, Note: *= Less than 0.05 |

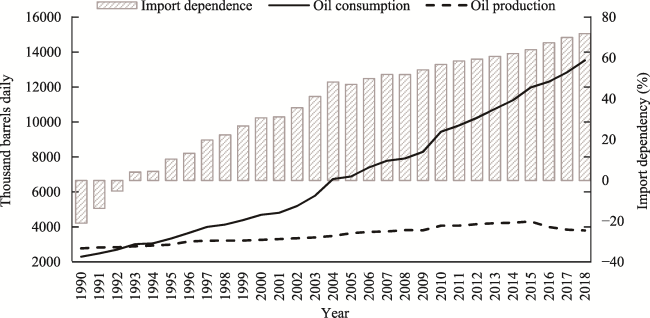

Figure 2 China’s import dependence for oil, 1990-2018Source: BP Statistical Review of World Energy June 2019 |

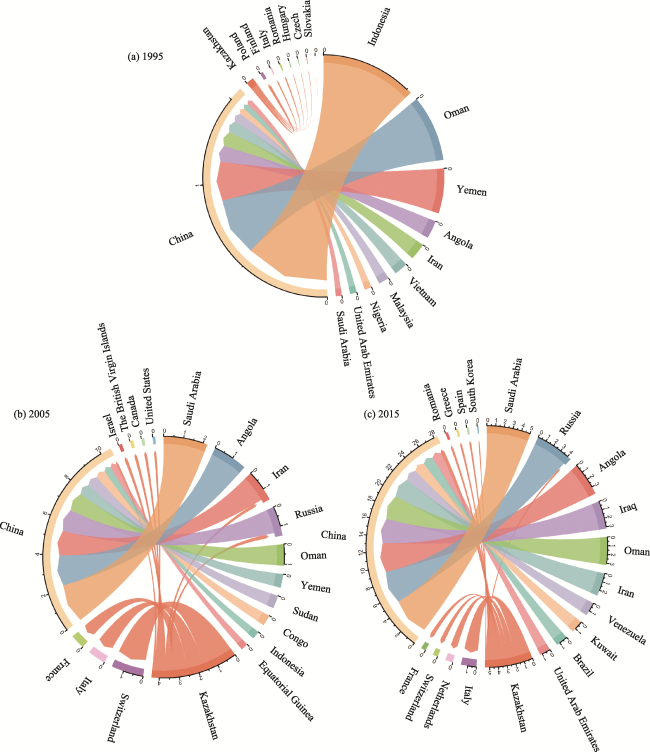

Figure 3 Trade in oil between China and Central Asian countries in 1995, 2005, and 2015 (10 million tons)Source: UN Comtrade website, https://comtrade.un.org/data/. |

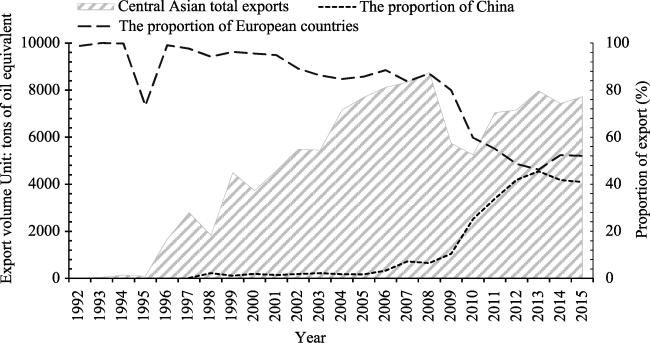

Figure 4 Changes in volumes and main export directions of Central AsiaSource: UN Comtrade website, https://comtrade.un.org/data/. |

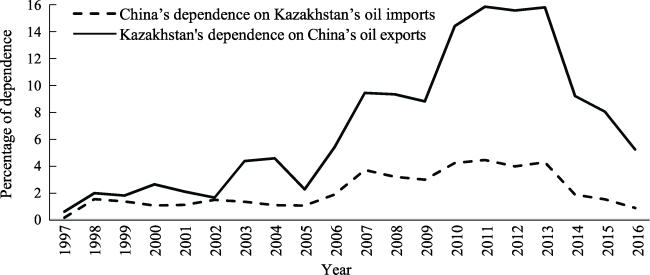

Figure 5 Oil trade interdependence between China and KazakhstanSource: UN Comtrade website, https://comtrade.un.org/data/. |

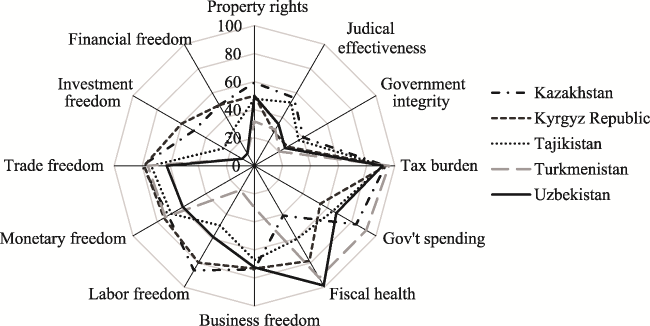

Figure 6 Economic freedom index values for five Central Asian countries |

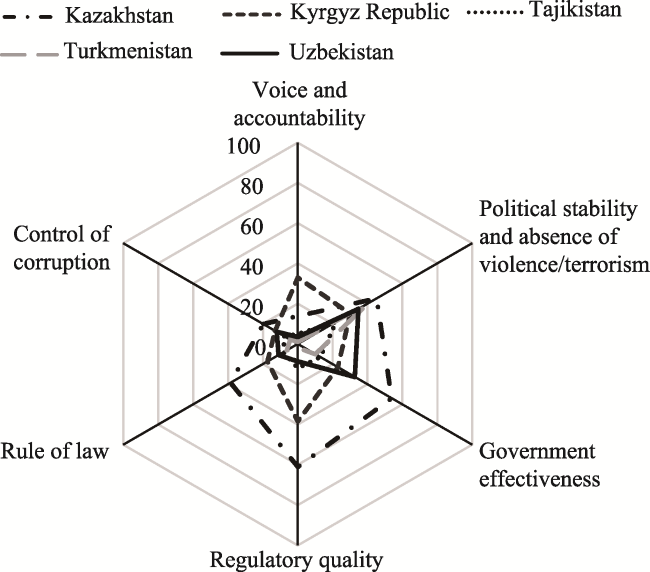

Figure 7 Global governance indicator rankings for Central Asia |

| 1 |

|

| 2 |

|

| 3 |

|

| 4 |

|

| 5 |

|

| 6 |

|

| 7 |

|

| 8 |

|

| 9 |

|

| 10 |

|

| 11 |

|

| 12 |

|

| 13 |

|

| 14 |

|

| 15 |

|

| 16 |

|

| 17 |

|

| 18 |

|

| 19 |

|

| 20 |

|

| 21 |

|

| 22 |

|

| 23 |

|

| 24 |

|

| 25 |

|

| 26 |

|

| 27 |

|

| 28 |

|

| 29 |

|

| 30 |

|

| 31 |

|

| 32 |

|

| 33 |

|

| 34 |

|

| 35 |

|

| 36 |

|

| 37 |

|

| 38 |

|

| 39 |

|

| 40 |

|

| 41 |

|

/

| 〈 |

|

〉 |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}