Journal of Geographical Sciences >

Chinese overseas ports: Market potential, supply capacity and access to imports

|

Dunford Michael, specialized in economic geography and regional development. E-mail: m.f.dunford@sussex.ac.uk |

Received date: 2020-03-22

Accepted date: 2020-06-16

Online published: 2020-10-27

Supported by

National Natural Science Foundation of China, No(41530751)

The Priority Research Program of Chinese Academy of Sciences, No(XDA19040403)

National Social Science Foundation of China, No(17VDL008)

Copyright

Especially since 2012 Chinese companies have acquired stakes as investors and constructors of overseas ports in both high-income and emerging economies. These initiatives play an important role in the construction of a Maritime Silk Road and China’s Belt and Road Initiative (BRI). Although a result of many factors, of which Chinese port investments are only one, macro-geographical gravity methods show that distance impedance and increases in the export market potential, export supply capacity and access to imports of these countries drove increases in income per capita. Export supply capacity rose particularly in Southeast Asia and more recently in Sub-Saharan Africa. In difficult times for the world economy, countries in which China invested in overseas port infrastructure saw increases in national export market potential and income per capita, due to reduction in the impedance of distance, while in the case of developing economies export market supply capacity and access to imported capital equipment and intermediate goods improved.

DUNFORD Michael , LIU Zhigao , XUE Jiashun . Chinese overseas ports: Market potential, supply capacity and access to imports[J]. Journal of Geographical Sciences, 2020 , 30(10) : 1681 -1701 . DOI: 10.1007/s11442-020-1807-7

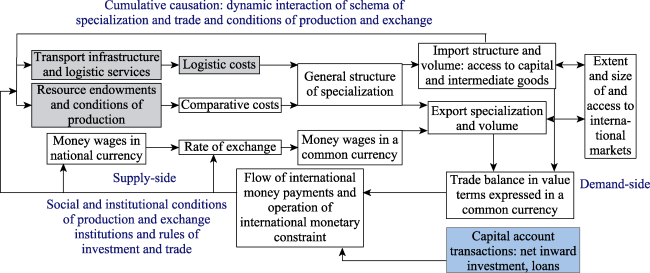

Figure 1 Cumulative causation: conditions of production and exchange, specialization, trade and investment(Source: elaborated from Dunford et al., 2014) |

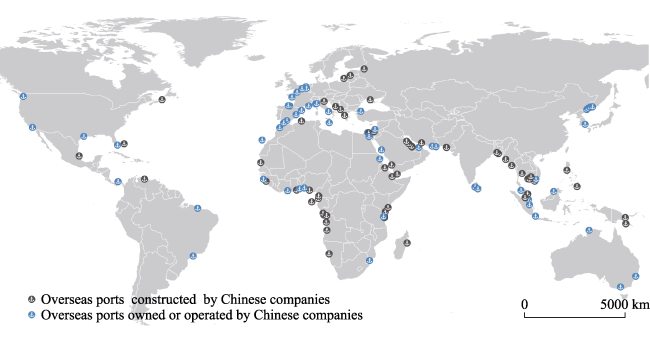

Figure 2 Overseas ports constructed or owned and operated by Chinese companies, 2017(Source: compiled by the authors from news and company reports) |

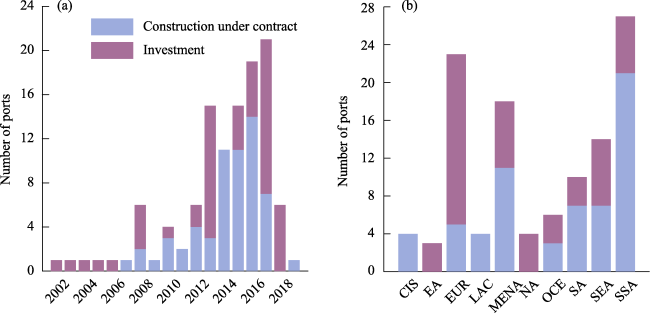

Figure 3 Evolution and geography of Chinese overseas ports(Source: Chinese ports database. Note: CIS=Commonwealth of Independent States; EA=East Asia; EUR=Europe; LAC=Latin America and the Caribbean; MENA=Middle East and North Africa; NA=North America; OCE=Oceania; SA=South Asia; SEA=Southeast Asia; SSA=Sub-Saharan Africa) |

Table 1 Gross domestic product, population and trade evolutions of countries with and without Chinese overseas ports (Source: elaborated from Chinese ports database, WITS and World Bank) |

| 2000 | 2008 | 2012 | 2017 | ||

|---|---|---|---|---|---|

| GDP share (%) | Construction contract | 15.0 | 15.5 | 15.5 | 14.9 |

| Investment | 42.5 | 40.3 | 38.9 | 37.7 | |

| Neither | 42.5 | 44.2 | 45.6 | 47.4 | |

| Population share (%) | Construction contract | 23.4 | 24.1 | 24.6 | 25.2 |

| Investment | 15.9 | 15.7 | 15.6 | 15.4 | |

| Neither | 60.7 | 60.1 | 59.8 | 59.4 | |

| GDP per capita (2010 USD) | Construction contract | 5202 | 6099 | 6153 | 6264 |

| Investment | 21690 | 24319 | 24482 | 25974 | |

| Neither | 5694 | 6966 | 7481 | 8472 | |

| Export share (%) | Construction contract | 19.7 | 18.2 | 17.5 | 17.3 |

| Investment | 34.3 | 34.5 | 35.8 | 35.8 | |

| Neither | 45.9 | 47.3 | 46.7 | 46.9 | |

| Import share (%) | Construction contract | 14.3 | 16.7 | 16.4 | 14.8 |

| Investment | 40.5 | 38.4 | 37.8 | 39.0 | |

| Neither | 45.1 | 44.9 | 45.8 | 46.3 | |

| 2008 | 2012 | 2014 | 2017 | ||

| Agriculture | Construction contract | 11.0 | 16.5 | 14.9 | 17.1 |

| Investment | 43.4 | 38.3 | 38.8 | 37.7 | |

| Neither | 45.6 | 45.2 | 46.3 | 45.2 | |

| Fuels | Construction contract | 46.8 | 49.4 | 46.7 | 38.6 |

| Investment | 23.0 | 22.4 | 22.8 | 26.5 | |

| Neither | 30.2 | 28.2 | 30.6 | 35.0 | |

| Manufactures | Construction contract | 9.4 | 10.5 | 10.5 | 10.7 |

| Investment | 33.1 | 29.9 | 29.9 | 28.5 | |

| Neither | 57.5 | 59.6 | 59.6 | 60.8 | |

| Ores and metals | Construction contract | 19.8 | 25.1 | 25.5 | 25.8 |

| Investment | 26.4 | 23.8 | 23.9 | 22.8 | |

| Neither | 53.7 | 51.1 | 50.5 | 51.4 | |

| Total exports | Construction contract | 15.8 | 18.3 | 17.4 | 14.7 |

| Investment | 32.6 | 30.0 | 30.1 | 29.4 | |

| Neither | 51.6 | 51.7 | 52.5 | 55.9 |

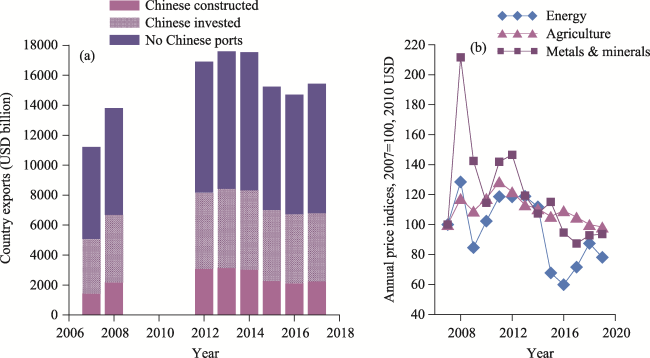

Figure 4 Evolution of world exports in countries with and without Chinese overseas ports and of nominal global commodity prices, 2007-2017(Source: trade data elaborated from World Bank, WITS, https://wits.worldbank.org/ and World Bank, commodity prices from http://www.worldbank.org/en/research/commodity-markets) |

Table 2 Estimating trade models for countries with Chinese overseas ports, 2008-2017 |

| Data used | Dependent variable | Year | Coefficients of distance | Adjusted R-squared | Reporter dummies (of 61 number not significant) | Partner dummies (of 205 number not significant) |

|---|---|---|---|---|---|---|

| Full trade matrix | ln(exports) | 2008 | -1.6537*** | 0.8813 | 15 | 0 |

| 2012 | -2.1889*** | 0.8948 | 1 | 0 | ||

| 2017 | -1.5850*** | 0.9025 | 18 | 0 | ||

| ln(imports) | 2008 | -1.5257*** | 0.8769 | 17 | 0 | |

| 2012 | -1.9156*** | 0.9050 | 6 | 0 | ||

| 2017 | -1.3294*** | 0.9030 | 14 | 1 | ||

| Revised trade matrix | ln(exports) | 2008 | -2.0107*** | 0.9691 | 12 | 0 |

| 2017 | -1.4228*** | 0.9706 | 14 | 0 | ||

| ln(imports) | 2008 | -1.5447*** | 0.9811 | 6 | 0 | |

| 2017 | -1.5160*** | 0.9806 | 0 | 0 |

*Significant at 10%, **Significant at 5%, ***significant at 1%. |

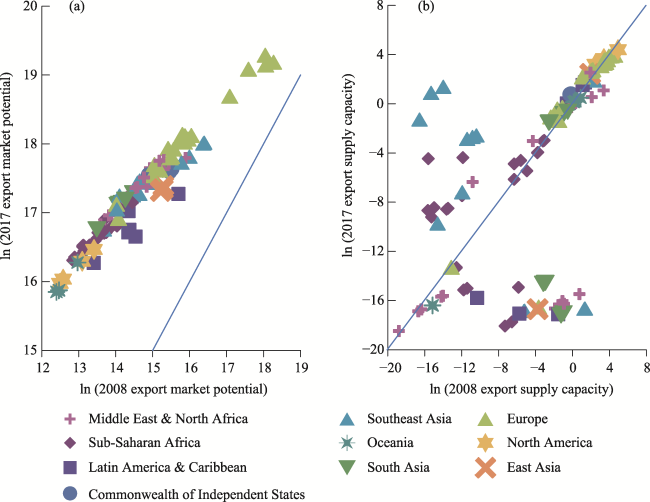

Figure 5 Foreign market potential and supply capacity of Chinese overseas ports, 2008 to 2017 |

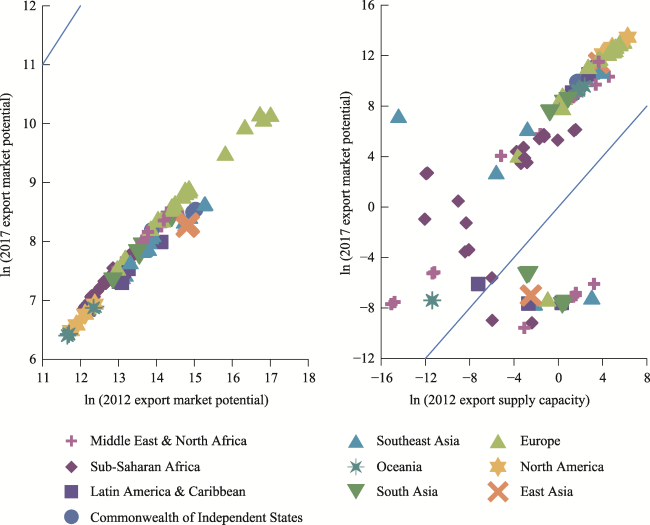

Figure 6 Foreign market potential and supply capacity of Chinese overseas ports, 2012 to 2017 |

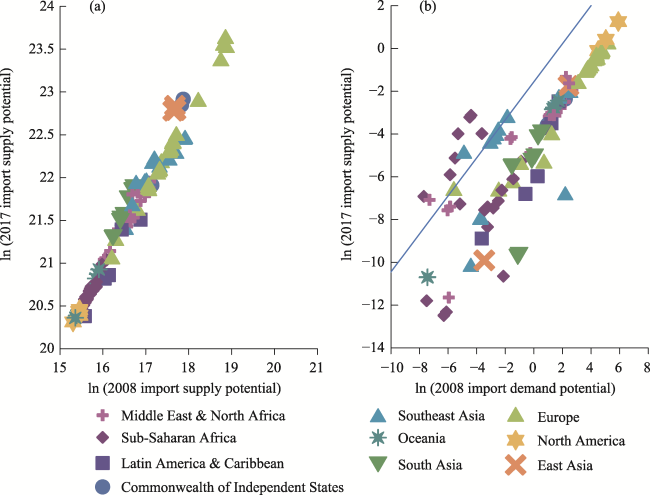

Figure 7 Import supply and demand potential, 2008-2017 |

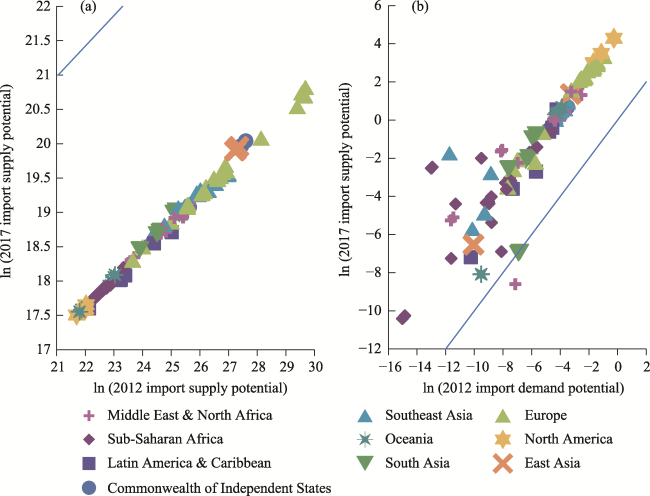

Figure 8 Import supply and demand potential, 2012-2017 |

Figure 9 Market potential, supply capacity and per capita GDP, 2017 |

Table 3 GDP per capita, market potential, supply capacity and foreign import access, 2017 |

| Export model | Import model | |

|---|---|---|

| ln (2017 Foreign market demand potential) | 0.486*** | |

| ln (2017 Foreign market supply capacity) | 0.059*** | |

| ln (2017 Foreign partner supply capacity) | 0.213 | |

| ln (2017 Foreign import access) | 0.300*** | |

| Constant | 4.542*** | 5.480** |

| F | 13.330*** | 42.110*** |

| R-squared | 0.204 | 0.447 |

*Significant at 10%, **significant at 5%, ***significant at 1% |

| 1 |

|

| 2 |

|

| 3 |

|

| 4 |

|

| 5 |

|

| 6 |

|

| 7 |

|

| 8 |

|

| 9 |

|

| 10 |

|

| 11 |

|

| 12 |

|

| 13 |

|

| 14 |

|

| 15 |

|

| 16 |

|

| 17 |

|

| 18 |

|

| 19 |

|

| 20 |

|

| 21 |

|

| 22 |

|

| 23 |

|

| 24 |

Office of the Leading Group for Promoting the Belt and Road Initiative (OLGPBRI), 2019. The Belt and Road Initiative: Progress, contributions and prospects.http://www.xinhuanet.com/2019-04/22/c_1124400071.htm

|

| 25 |

|

| 26 |

|

| 27 |

|

| 28 |

|

| 29 |

|

| 30 |

|

| 31 |

|

| 32 |

|

| 33 |

|

| 34 |

|

| 35 |

UNCTAD, 2019. Review of maritime transport 2018. https://unctad.org/en/pages/PublicationWebflyer.aspx?publicationid=2245

|

| 36 |

|

| 37 |

|

/

| 〈 |

|

〉 |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}