Journal of Geographical Sciences >

Does geographic distance have a significant impact on enterprise financing costs?

|

Sun Wei (1975─), Associate Professor, specialized in regional development and spatial planning. E-mail: sunw@igsnrr.ac.cn |

Received date: 2019-05-30

Accepted date: 2019-07-29

Online published: 2019-12-06

Supported by

Strategic Priority Research Program of the Chinese Academy of Sciences, No(XDA19040401)

Youth Fund for Humanities and Social Sciences of the Ministry of Education of China, No(16YJCZH040)

Youth Fund for Humanities and Social Sciences of the Ministry of Education of China, No(14YJCZH078)

National Natural Science Foundation of China, No(41571117)

National Natural Science Foundation of China, No(41871117)

Social Science Foundation of Beijing, No(14CSB010)

Shandong Taishan Scholar Youth Expert Support Program

Copyright

As information technology has been applied more broadly and transportation infrastructure has improved, persistent debate has existed as to the question of whether geographic distance influences enterprise financing costs (EFCs). Through mining big data regarding industrial enterprises and commercial bank branches (CBBs) in the Beijing-Tianjin-Hebei region, this paper conducts quantitative analysis of correlation between the EFCs and their distance to CBBs as well as the number of CBBs within a 1-5 km radius, and investigates how geographic factors affect EFCs. The results indicate the following: (1) In overall terms, the shorter the distance to CBBs and the greater the number of CBBs within a 1-5 km radius, the lower the EFCs. (2) Distance to CBBs and number of CBBs within a 1-5 km radius significantly influence state-owned and non-state-owned enterprises, with the effect on non-state-owned enterprises being more pronounced. (3) The EFCs in Beijing and Tianjin are not correlated with distance to CBBs, and negatively correlated to the number of CBBs within a 1-5 km radius; the EFCs in Hebei Province are positively correlated with distance to CBBs, and negatively correlated with the number of CBBs within a 1-5 km radius. (4) Distance to CBBs has a more significant impact on enterprises engaged in heavy industry and labor-intensive industries, while there is not much difference between different industries in terms of how the number of CBBs within a 1-5 km radius affects them.

SUN Wei , LI Qihang , LI Bo . Does geographic distance have a significant impact on enterprise financing costs?[J]. Journal of Geographical Sciences, 2019 , 29(12) : 1965 -1980 . DOI: 10.1007/s11442-019-1699-6

Table 1 Definition and explanation of variables |

| Variable category | Explanation |

|---|---|

| lfcost_r | Natural logarithm of EFCs obtained by retaining positive values from dividing interest expenses by the difference between total liabilities and accounts payable, winsorized at top and bottom 1% |

| distance | Natural logarithm of the mean distance to the three closest CBBs to the enterprise |

| num_1k | Number of CBBs within a 1 km radius from the enterprise |

| num_3k | Number of CBBs within a 3 km radius from the enterprise |

| num_5k | Number of CBBs within a 5 km radius from the enterprise |

| lfa | Natural logarithm of fixed assets |

| lwc | Natural logarithm of operating capital |

| lworker | Natural logarithm of number of employees |

| lev | Leverage ratio (assets divided by liabilities) |

| dum_gov | SOE dummy variable (has a value of 1 if state-owned shares account for more than 50% of paid-in capital, otherwise has a value of 0) |

| dum_for | Foreign enterprise dummy variable (has a value of 1 if foreign capital shares (includes Hong Kong, Macao, and Taiwan) account for more than 25% of paid-in capital, otherwise has a value of 0) |

| dum_qg | Light industry dummy variable (has a value of 1 if the industry fits in to the light category as defined by the national bureau of statistics, and a value of 0 if it fits into the heavy category) |

| dum_lab | Labor intensive industry dummy variable (has a value of 1 if the ratio between number of workers and output value for industry as a whole is above the median of the same ratio for all industries, otherwise has a value of 0) |

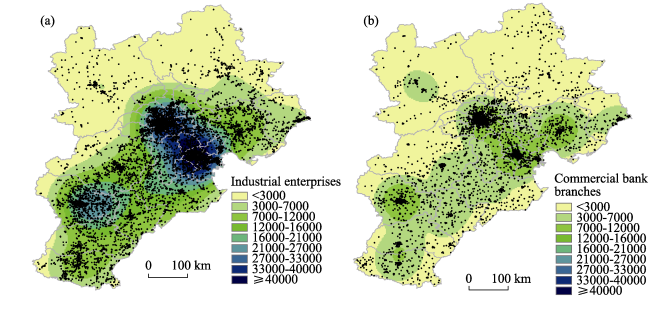

Figure 1 Kernel density estimation map for industrial enterprises (a) and banks (b) in the Beijing-Tianjin-Hebei region in 2013 |

Table 2 Correlation coefficients of variables |

| lfcost_r | distance | Num_1k | Num_3k | Num_5k | lfa | lev | |

|---|---|---|---|---|---|---|---|

| distance | 0.086*** | 1 | |||||

| Num_1k | -0.082*** | -0.507*** | 1 | ||||

| Num_3k | -0.136*** | -0.274*** | 0.769*** | 1 | |||

| Num_5k | -0.149*** | -0.213*** | 0.672*** | 0.955*** | 1 | ||

| lfa | 0.140*** | -0.013 | 0.028*** | 0.015* | -0.003 | 1 | |

| lev | -0.216*** | -0.063*** | 0.021*** | 0.037*** | 0.039*** | -0.099*** | 1 |

Note: The *, **, and *** symbols represent 10%, 5%, and 1% levels of significance, respectively |

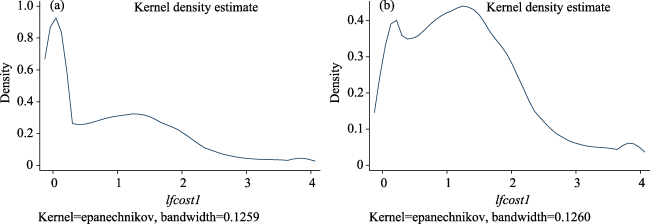

Figure 2 Kernel density estimation of financing cost logarithms with the full sample (a) and with zero values eliminated (b) |

Table 3 Results of OLS regression and Tobit regression of EFCs and other variables |

| Variables | Regression (1) | Regression (2) | Regression (3) | Regression (4) | Regression (5) | Regression (6) |

|---|---|---|---|---|---|---|

| OLS | OLS | OLS | Tobit | Tobit | Tobit | |

| distance | 0.020** | 0.018*** | 0.019*** | 0.022*** | 0.019*** | 0.021*** |

| (2.69) | (3.26) | (3.32) | (3.17) | (3.07) | (3.34) | |

| num_1k | -0.004 | -0.005 | ||||

| (-1.17) | (-1.31) | |||||

| num_3k | -0.002*** | -0.003*** | ||||

| (-4.01) | (-4.58) | |||||

| num_5k | -0.001*** | -0.001*** | ||||

| (-3.69) | (-5.08) | |||||

| lfa | 0.110*** | 0.107*** | 0.106*** | 0.176*** | 0.171*** | 0.170*** |

| (5.90) | (5.73) | (5.80) | (13.54) | (13.11) | (13.01) | |

| lwc | -0.081 | -0.076 | -0.075 | -0.055*** | -0.047*** | -0.046*** |

| (-1.54) | (-1.48) | (-1.47) | (-3.50) | (-3.00) | (-2.91) | |

| lworker | 0.009 | 0.012 | 0.013 | 0.004 | 0.008 | 0.009 |

| (0.32) | (0.42) | (0.43) | (0.19) | (0.40) | (0.43) | |

| lev | -1.034* | -1.025* | -1.024* | -0.855*** | -0.843*** | -0.840*** |

| (-2.00) | (-2.00) | (-2.00) | (-12.34) | (-12.16) | (-12.13) | |

| dum_gov | 0.175* | 0.182** | 0.184** | 0.287*** | 0.299*** | 0.301*** |

| (2.08) | (2.21) | (2.22) | (6.16) | (6.40) | (6.45) | |

| dum_for | -0.065 | -0.069 | -0.070 | -0.084** | -0.090** | -0.092** |

| (-1.10) | (-1.23) | (-1.26) | (-2.14) | (-2.30) | (-2.35) | |

| City effects | YES | YES | YES | YES | YES | YES |

| Industry effects | YES | YES | YES | YES | YES | YES |

| City cluster-robust standard errors | YES | YES | YES | - | - | - |

| _cons | 2.042** | 2.014** | 1.999** | 0.938*** | 0.902*** | 0.879*** |

| (2.97) | (2.95) | (2.94) | (4.03) | (3.89) | (3.79) | |

| N | 11780 | 11780 | 11780 | 15987 | 15987 | 15987 |

| Adjusted R2 | 0.225 | 0.226 | 0.226 |

Note: Numbers in brackets are the t values of regression coefficients. The *, **, and *** symbols represent 10%, 5%, and 1% significance levels, respectively. |

Table 4 Results of OLS regression of EFCs (sample divided by provincial unit) |

| Variables | Regression (1) | Regression (2) | Regression (3) | Regression (4) | Regression (5) | Regression (6) |

|---|---|---|---|---|---|---|

| Beijing-Tianjin OLS | Hebei OLS | Beijing-Tianjin OLS | Hebei OLS | Beijing-Tianjin OLS | Hebei OLS | |

| distance | 0.00537 | 0.0216 | 0.00526 | 0.0192** | 0.00643 | 0.0213** |

| (2.188) | (1.147) | (1.903) | (2.323) | (3.250) | (2.659) | |

| num_1k | -0.00535*** | -0.00738 | ||||

| (-78.62) | (-0.417) | |||||

| num_3k | -0.00149** | -0.00462*** | ||||

| (-20.96) | (-4.863) | |||||

| num_5k | -0.000590 | -0.00225*** | ||||

| (-4.994) | (-3.506) | |||||

| lfa | 0.0666* | 0.0755** | 0.0644* | 0.0712** | 0.0645* | 0.0695** |

| (9.409) | (2.634) | (10.28) | (2.531) | (11.84) | (2.539) | |

| lwc | -0.0867 | -0.218*** | -0.0835 | -0.210*** | -0.0836 | -0.208*** |

| (-1.801) | (-9.332) | (-1.770) | (-9.123) | (-1.810) | (-9.167) | |

| lworker | -0.00807 | 0.0489 | -0.00624 | 0.0563 | -0.00594 | 0.0569 |

| (-0.474) | (1.156) | (-0.389) | (1.390) | (-0.384) | (1.428) | |

| lev | -0.828 | -2.463*** | -0.825 | -2.433*** | -0.825 | -2.424*** |

| (-3.177) | (-13.02) | (-3.244) | (-13.17) | (-3.243) | (-13.47) | |

| dum_gov | -0.0590 | -0.103 | -0.0610 | -0.102 | -0.0623 | -0.102 |

| (-0.691) | (-0.930) | (-0.731) | (-0.926) | (-0.756) | (-0.918) | |

| City effects | YES | YES | YES | YES | YES | YES |

| Industry effects | YES | YES | YES | YES | YES | YES |

| City cluster-robust standard errors | YES | YES | YES | YES | YES | YES |

| _cons | 2.358 | 4.775*** | 2.350 | 4.699*** | 2.328 | 4.663*** |

| (2.087) | (11.56) | (2.053) | (12.44) | (2.039) | (12.10) | |

| N | 3752 | 5533 | 3752 | 5533 | 3752 | 5533 |

| Adjusted R2 | 0.073 | 0.206 | 0.0748 | 0.207 | 0.075 | 0.208 |

Note: Numbers in brackets are the t values of regression coefficients. The *, **, and *** symbols represent 10%, 5%, and 1% significance levels, respectively. |

Table 5 Results of OLS regression of EFCs (sample divided according to the light and heavy industry categories) |

| Variables | Regression (1) | Regression (2) | Regression (3) | Regression (4) | Regression (5) | Regression (6) |

|---|---|---|---|---|---|---|

| Light industry OLS | Heavy industry OLS | Light industry OLS | Heavy industry OLS | Light industry OLS | Heavy industry OLS | |

| distance | 0.0146 | 0.0224* | 0.00781 | 0.0244** | 0.00936 | 0.0260** |

| (1.134) | (2.053) | (1.135) | (2.835) | (1.344) | (2.988) | |

| num_1k | 0.00157 | -0.00819 | ||||

| (0.159) | (-1.516) | |||||

| num_3k | -0.00268*** | -0.00211*** | ||||

| (-5.250) | (-3.742) | |||||

| num_5k | 0.00109*** | -0.000850*** | ||||

| (-4.154) | (-3.578) | |||||

| lfa | 0.0728** | 0.0839*** | 0.0677* | 0.0815*** | 0.0672* | 0.0814*** |

| (2.247) | (5.488) | (2.098) | (5.628) | (2.106) | (5.739) | |

| lwc | -0.186*** | -0.180*** | -0.175*** | -0.176*** | -0.175*** | -0.176*** |

| (-3.660) | (-5.151) | (-3.530) | (-5.143) | (-3.625) | (-5.178) | |

| lworker | 0.0368 | 0.0229 | 0.0415 | 0.0255 | 0.0410 | 0.0254 |

| (1.186) | (0.566) | (1.313) | (0.632) | (1.298) | (0.635) | |

| lev | -2.266*** | -1.853*** | -2.252*** | -1.842*** | -2.253*** | -1.842*** |

| (-5.049) | (-5.830) | (-5.084) | (-5.869) | (-5.114) | (-5.872) | |

| Dum_gov | -0.0859 | -0.0855 | -0.0882 | -0.0861 | -0.0877 | -0.0870 |

| (-1.130) | (-1.167) | (-1.209) | (-1.196) | (-1.228) | (-1.216) | |

| City effects | YES | YES | YES | YES | YES | YES |

| Industry effects | YES | YES | YES | YES | YES | YES |

| City cluster-robust standard errors | YES | YES | YES | YES | YES | YES |

| _cons | 4.283*** | 4.052*** | 4.270*** | 3.998*** | 4.262*** | 3.982*** |

| (8.526) | (7.664) | (8.215) | (7.940) | (8.325) | (7.928) | |

| N | 2317 | 6968 | 2317 | 6968 | 2317 | 6968 |

| Adjusted R2 | 0.268 | 0.181 | 0.269 | 0.182 | 0.269 | 0.182 |

Note: Numbers in brackets are the t values of regression coefficients. The *, **, and *** symbols represent 10%, 5%, and 1% significance levels, respectively. |

Table 6 Results of OLS regression of EFCs (sample divided according to labor-intensive industry and non-labor intensive industry categories) |

| Variables | Regression (1) | Regression (2) | Regression (3) | Regression (4) | Regression (5) | Regression (6) |

|---|---|---|---|---|---|---|

| Intensive OLS | Non-intensive OLS | Intensive OLS | Non-intensive OLS | Intensive OLS | Non-intensive OLS | |

| distance | 0.0235** | 0.0155 | 0.0239*** | 0.0152 | 0.0259*** | 0.0163 |

| (2.900) | (1.337) | (4.335) | (1.550) | (4.416) | (1.666) | |

| num_1k | -0.00831 | -0.00389 | ||||

| (-1.509) | (-0.781) | |||||

| num_3k | -0.00275*** | -0.00162** | ||||

| (-4.603) | (-2.808) | |||||

| num_5k | -0.00107*** | -0.000660** | ||||

| (-3.733) | (-2.778) | |||||

| lfa | 0.0712** | 0.0876*** | 0.0674** | 0.0850*** | 0.0671** | 0.0850*** |

| (2.625) | (3.570) | (2.508) | (3.556) | (2.522) | (3.588) | |

| lwc | -0.177*** | -0.181*** | -0.170*** | -0.177*** | -0.171*** | -0.177*** |

| (-4.226) | (-5.142) | (-4.144) | (-5.133) | (-4.205) | (-5.197) | |

| lworker | 0.0312 | 0.0162 | 0.0343 | 0.0188 | 0.0339 | 0.0188 |

| (0.875) | (0.496) | (0.952) | (0.583) | (0.953) | (0.587) | |

| lev | -2.106*** | -1.838*** | -2.091*** | -1.830*** | -2.091*** | -1.829*** |

| (-5.469) | (-5.420) | (-5.501) | (-5.458) | (-5.515) | (-5.470) | |

| Dum_gov | -0.105 | -0.0680 | -0.105 | -0.0699 | -0.106 | -0.0700 |

| (-1.533) | (-0.981) | (-1.562) | (-1.033) | (-1.607) | (-1.039) | |

| City effects | YES | YES | YES | YES | YES | YES |

| Industry effects | YES | YES | YES | YES | YES | YES |

| City cluster-robust standard errors | YES | YES | YES | YES | YES | YES |

| _cons | 3.128*** | 3.965*** | 3.078*** | 3.937*** | 3.066*** | 3.925*** |

| (4.747) | (7.532) | (4.770) | (7.686) | (4.754) | (7.681) | |

| N | 4201 | 5084 | 4201 | 5084 | 4201 | 5084 |

| Adjusted R2 | 0.226 | 0.197 | 0.228 | 0.198 | 0.228 | 0.198 |

Note: Numbers in brackets are the t values of regression coefficients. The *, **, and *** symbols represent 10%, 5%, and 1% significance levels, respectively. |

Table 7 Results of OLS and IV-2SLS regression of EFCs |

| Variables | Regression (1) | Regression (2) | Regression (3) | Regression (4) |

|---|---|---|---|---|

| OLS | IV | IV | IV | |

| ldis | 0.074*** | 0.698*** | 0.374** | 0.377** |

| (6.67) | (3.78) | (2.56) | (2.36) | |

| lfa | 0.105*** | 0.069*** | 0.071*** | |

| (9.57) | (2.65) | (2.94) | ||

| lwc | -0.091** | -0.038 | -0.027 | |

| (-2.30) | (-0.83) | (-0.64) | ||

| lworker | 0.039 | 0.076* | 0.055* | |

| (1.43) | (1.74) | (1.75) | ||

| lev | -0.951** | -0.837*** | -0.755*** | |

| (-2.95) | (-2.93) | (-3.05) | ||

| dum_gov | 0.438*** | 0.435*** | 0.389*** | |

| (6.77) | (4.46) | (4.59) | ||

| dum_for | -0.019 | -0.044 | -0.049** | |

| (-0.43) | (-1.64) | (-2.18) | ||

| _cons | 0.828 | -4.352*** | -2.343* | -2.043 |

| (1.50) | (-3.33) | (-1.84) | (-1.45) | |

| IV | No | Yes | Yes | Yes |

| Fixed effects | Yes | No | No | Yes |

| Cluster-robust | Yes | Yes | Yes | Yes |

| N | 14845 | 14845 | 14845 | 14845 |

| Adjusted R2 | 0.243 | -0.383 | 0.093 | 0.132 |

| Weak instruments test | 12.343 | 8.135 | 9.799 | |

| Overidentification test | 3.260 | 3.691 | 5.361 | |

| 0.196 | 0.158 | 0.069 | ||

| Endogeneity test | 5.653 | 3.183 | 1.753 | |

| 0.019 | 0.078 | 0.215 |

Note: Numbers in brackets are the t values of regression coefficients. The *, **, and *** symbols represent 10%, 5%, and 1% significance levels, respectively. |

| 1 |

|

| 2 |

|

| 3 |

|

| 4 |

|

| 5 |

|

| 6 |

|

| 7 |

|

| 8 |

|

| 9 |

|

| 10 |

|

| 11 |

|

| 12 |

|

/

| 〈 |

|

〉 |

{kind=link}

{kind=link}

{kind=link}

{kind=link}